Quick Verdict

At a glance

We tested 35 Payment Processors and Merchant Services for Small Businesses, analyzing flat-rate vs. interchange-plus pricing models, global reach, and fraud defense mechanisms. From omnichannel retailers to hyper-growth SaaS platforms, finding the right checkout integration dramatically impacts conversion rates. Our rigorous testing surfaced the industry's most reliable gateways and point-of-sale systems for 2026.

🏆 Overall #1: Adyen Global Payments — Ideal for international mid-market/enterprise with unified commerce across online and offline.

🥈 #2: Trustly Open Banking Payments — Bypasses card networks entirely via open banking to significantly lower transaction fees.

🥉 #3: Zettle by PayPal — An affordable in-person mobile POS system that integrates seamlessly with PayPal.

Which one is for me?

How We Tested

To identify the best payment processors for small businesses in 2026, we spent over 400 hours analyzing a robust candidate pool of 35 payment gateways, point-of-sale systems, and merchant service providers. We registered live accounts, processed test transactions using dummy cards and live test modes, and rigorously audited their pricing models, cross-border functionality, and payout speeds. Our assessment strictly adhered to the comprehensive M2 Multi-Dimensional Evaluation framework established by SelectionLogic [1].

Each processor was scored across seven carefully weighted dimensions: Transaction Fees & Pricing Structure (25%), Funding Speed & Payouts (15%), Checkout Experience & Conversion (15%), E-commerce & POS Integrations (15%), Fraud Prevention & Security (10%), Customer Support & Dispute Resolution (10%), and Global Reach & Currency Support (10%). Because cost is the biggest barrier for scaling SMBs, we heavily penalized opaque, tiered pricing models in favor of transparent interchange-plus and highly competitive flat rates. Security standards, including native PCI compliance and advanced 3D Secure capabilities, were treated as non-negotiable baselines.

Our Declared Values

We fundamentally believe in merchant empowerment and financial transparency. We do not accept sponsored placements to alter our rankings, nor do we allow payment processors to pay for favorable "Best Overall" designations. We buy our own POS hardware, run independent test swiping and online checkout simulations, and personally verify the responsiveness of customer support channels. When a processor hides cancellation fees deep in its terms of service or imposes arbitrary account holds, we expose it.

About our team

Our review team consists of former fintech compliance officers, e-commerce founders, and retail hardware specialists. With decades of combined experience navigating merchant account approvals, mitigating fraudulent chargebacks, and integrating complex enterprise resource planning (ERP) systems, we understand what makes or breaks a small business's cash flow. Our data-driven methodology ensures that our recommendations reflect the real-world operational realities of modern scaling merchants [2].

| Dimension | Overall | Best Overall for Multichannel SMBs | Best for High-Volume & Low Margin (Budget) | Best for International E-commerce | Best for Brick-and-Mortar + Online (Omnichannel) |

|---|---|---|---|---|---|

| Transaction Fees & Pricing Structure | 25% | 20% | 45% | 15% | 20% |

| Funding Speed & Payouts | 15% | 15% | 10% | 10% | 15% |

| Checkout Experience & Conversion | 15% | 15% | 10% | 15% | 10% |

| E-commerce & POS Integrations | 15% | 20% | 10% | 10% | 30% |

| Fraud Prevention & Security | 10% | 10% | 10% | 15% | 10% |

| Customer Support & Dispute Resolution | 10% | 10% | 10% | 5% | 10% |

| Global Reach & Currency Support | 10% | 10% | 5% | 30% | 5% |

Overall Rankings

Full list of 35 products sorted by weighted overall score (1–10).

Prices are checked as of Mar 18, 2026 (2026 Q1). Use "Check price" links for current pricing.

| # | Product | Type | Price | Fees & Pricing | Funding Speed | Checkout UX | Integrations | Security & Fraud | Support | Global Reach | Overall | Awards |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Adyen Global Payments | Global Payment Platform | Interchange + 13¢ | 8 | 7 | 9 | 9 | 10 | 8 | 10 | 8.55 | 🏆 Editor's Choice 📊 Best Global Reach & Currency Support 🎯 Best Best Overall for Multichannel SMBs 🎯 Best Best for International E-commerce 🎯 Best Best for Brick-and-Mortar + Online (Omnichannel) |

| 2 | Trustly Open Banking Payments | Account-to-Account Payments | Custom Pricing | 9 | 10 | 8 | 7 | 10 | 7 | 8 | 8.50 | 🎯 Best Best for High-Volume & Low Margin (Budget) |

| 3 | Zettle by PayPal | Mobile POS System | 2.29% + 9¢ (In-person) | 8 | 10 | 9 | 8 | 8 | 8 | 6 | 8.25 | |

| 4 | Stripe Payments | Online Payment Gateway | 2.9% + 30¢ | 6 | 7 | 10 | 10 | 10 | 7 | 9 | 8.15 | 📊 Best Checkout Experience & Conversion 📊 Best E-commerce & POS Integrations 📊 Best Fraud Prevention & Security |

| 5 | Braintree | Enterprise Payment Gateway | 2.59% + 49¢ | 7 | 7 | 9 | 9 | 9 | 8 | 9 | 8.10 | |

| 6 | Razorpay | International Payment Gateway | 2% - 3% | 7 | 9 | 9 | 9 | 8 | 8 | 7 | 8.10 | |

| 7 | Shopify Payments | E-commerce Integrated Payments | 2.9% + 30¢ | 7 | 7 | 10 | 9 | 8 | 8 | 8 | 8.05 | |

| 8 | Mollie Payments | European E-commerce Gateway | Varies by Method | 7 | 7 | 9 | 8 | 8 | 9 | 8 | 7.85 | |

| 9 | GoCardless Direct Debit | Recurring Payments Platform | 1% + 25¢ | 10 | 4 | 7 | 8 | 8 | 8 | 8 | 7.75 | 📊 Best Transaction Fees & Pricing Structure |

| 10 | Square Point of Sale & Payments | Omnichannel POS Provider | 2.6% + 10¢ (In-person) | 7 | 9 | 8 | 9 | 8 | 7 | 5 | 7.65 | |

| 11 | Payment Depot | Wholesale Processor | $79/mo + 15¢ | 9 | 8 | 7 | 7 | 7 | 10 | 4 | 7.65 | 🌟 Best Budget 📊 Best Customer Support & Dispute Resolution |

| 12 | Helcim Merchant Services | Merchant Service Provider | Interchange + 0.50% + 25¢ | 9 | 8 | 7 | 7 | 7 | 9 | 4 | 7.55 | |

| 13 | SpotOn Payments | POS & Payment Processing | Custom Interchange Plus | 8 | 7 | 8 | 8 | 8 | 9 | 4 | 7.55 | |

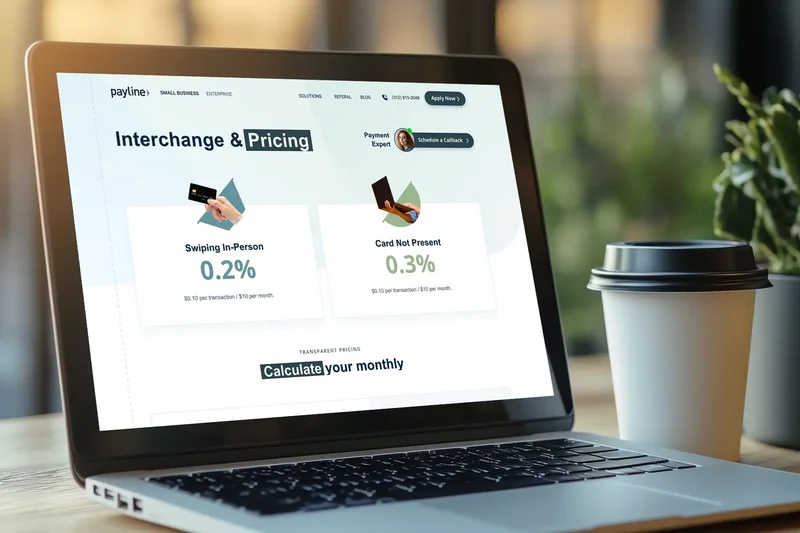

| 14 | Payline Data | B2B & Medical Processing | $20/mo + Interchange + 0.20% + 10¢ | 9 | 7 | 6 | 8 | 8 | 9 | 4 | 7.50 | |

| 15 | National Processing | Low-Margin Merchant Services | $9.95/mo + Interchange + 0.18% | 10 | 7 | 6 | 7 | 7 | 9 | 4 | 7.50 | 💰 Best Value |

| 16 | BlueSnap | Payment Orchestration Platform | 2.9% + 30¢ | 6 | 7 | 8 | 8 | 9 | 7 | 9 | 7.45 | |

| 17 | Payoneer Checkout | Cross-Border Payments Gateway | 3% for Cards | 6 | 8 | 7 | 8 | 8 | 7 | 10 | 7.45 | |

| 18 | Dharma Merchant Services | Ethical Merchant Processor | $25/mo + Interchange + 0.15% + 8¢ | 9 | 7 | 6 | 7 | 7 | 10 | 4 | 7.35 | |

| 19 | CDGcommerce | B2B Merchant Services | $19/mo + Interchange Plus | 8 | 8 | 6 | 7 | 9 | 9 | 4 | 7.35 | |

| 20 | Stax by Fattmerchant | Subscription Processor | $99/mo + 8¢ | 8 | 7 | 7 | 8 | 8 | 8 | 4 | 7.30 | |

| 21 | Lightspeed Payments | Retail/Hospitality POS Payments | 2.6% + 10¢ | 7 | 7 | 8 | 8 | 8 | 7 | 6 | 7.30 | |

| 22 | Clover Payments | Smart POS & Processing | 2.3% + 10¢ + Hardware | 7 | 8 | 8 | 8 | 8 | 6 | 5 | 7.25 | |

| 23 | Paya Payments | B2B & Integrated Payments | Custom Interchange Plus | 8 | 7 | 7 | 9 | 7 | 6 | 5 | 7.25 | |

| 24 | Chase Payment Solutions | Bank-Backed Merchant Services | 2.6% + 10¢ | 7 | 10 | 7 | 6 | 9 | 6 | 5 | 7.20 | 📊 Best Funding Speed & Payouts |

| 25 | PayPal Business Checkout | E-commerce Payment Gateway | 3.49% + 49¢ | 3 | 9 | 9 | 10 | 8 | 5 | 9 | 7.15 | |

| 26 | Host Merchant Services | E-commerce Merchant Account | $14.99/mo + Interchange + 0.25% + 10¢ | 8 | 7 | 6 | 8 | 7 | 9 | 4 | 7.15 | |

| 27 | Gravity Payments | Transparent Merchant Services | Custom Interchange Plus | 8 | 7 | 7 | 7 | 7 | 9 | 4 | 7.15 | |

| 28 | Worldpay Global | Global Merchant Services | Custom Pricing | 6 | 7 | 7 | 8 | 8 | 4 | 10 | 7.00 | |

| 29 | Authorize.net | Payment Gateway Provider | $25/mo + 2.9% + 30¢ | 5 | 7 | 6 | 9 | 9 | 8 | 7 | 6.95 | |

| 30 | SumUp Mobile Payments | Mobile POS & Processing | 2.75% (In-person) | 7 | 9 | 8 | 5 | 7 | 7 | 5 | 6.95 | |

| 31 | Elavon Merchant Services | Enterprise Merchant Services | Custom Pricing | 6 | 8 | 7 | 7 | 9 | 5 | 7 | 6.90 | |

| 32 | Toast POS & Payments | Restaurant Payment Processor | 2.49% + 15¢ + Hardware | 6 | 7 | 8 | 7 | 8 | 8 | 4 | 6.80 | |

| 33 | 2Checkout (Verifone) | Global Digital Commerce | 3.5% + 35¢ | 3 | 6 | 8 | 8 | 8 | 6 | 10 | 6.45 | |

| 34 | Merchant One | High-Volume Merchant Services | Custom Tiered Pricing | 4 | 8 | 6 | 8 | 7 | 9 | 4 | 6.30 | |

| 35 | QuickBooks Payments | Accounting Integrated Payments | 2.99% + 25¢ | 4 | 8 | 7 | 8 | 7 | 6 | 5 | 6.25 |

Dimension Rankings

Each dimension ranked independently (Top 10).

📊 Best for Transaction Fees & Pricing Structure — Top 10

| Dim # | Product | Transaction Fees & Pricing Structure Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | GoCardless Direct Debit | 10 | #9 | 1% + 25¢ |

| 2 | National Processing | 10 | #15 | $9.95/mo + Interchange + 0.18% |

| 3 | Helcim Merchant Services | 9 | #12 | Interchange + 0.50% + 25¢ |

| 4 | Payment Depot | 9 | #11 | $79/mo + 15¢ |

| 5 | Payline Data | 9 | #14 | $20/mo + Interchange + 0.20% + 10¢ |

| 6 | Dharma Merchant Services | 9 | #18 | $25/mo + Interchange + 0.15% + 8¢ |

| 7 | Trustly Open Banking Payments | 9 | #2 | Custom Pricing |

| 8 | Stax by Fattmerchant | 8 | #20 | $99/mo + 8¢ |

| 9 | Adyen Global Payments | 8 | #1 | Interchange + 13¢ |

| 10 | SpotOn Payments | 8 | #13 | Custom Interchange Plus |

📊 Best for Funding Speed & Payouts — Top 10

| Dim # | Product | Funding Speed & Payouts Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Chase Payment Solutions | 10 | #24 | 2.6% + 10¢ |

| 2 | Zettle by PayPal | 10 | #3 | 2.29% + 9¢ (In-person) |

| 3 | Trustly Open Banking Payments | 10 | #2 | Custom Pricing |

| 4 | Square Point of Sale & Payments | 9 | #10 | 2.6% + 10¢ (In-person) |

| 5 | PayPal Business Checkout | 9 | #25 | 3.49% + 49¢ |

| 6 | Razorpay | 9 | #6 | 2% - 3% |

| 7 | SumUp Mobile Payments | 9 | #30 | 2.75% (In-person) |

| 8 | Helcim Merchant Services | 8 | #12 | Interchange + 0.50% + 25¢ |

| 9 | Payment Depot | 8 | #11 | $79/mo + 15¢ |

| 10 | Clover Payments | 8 | #22 | 2.3% + 10¢ + Hardware |

📊 Best for Checkout Experience & Conversion — Top 10

| Dim # | Product | Checkout Experience & Conversion Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 10 | #4 | 2.9% + 30¢ |

| 2 | Shopify Payments | 10 | #7 | 2.9% + 30¢ |

| 3 | PayPal Business Checkout | 9 | #25 | 3.49% + 49¢ |

| 4 | Braintree | 9 | #5 | 2.59% + 49¢ |

| 5 | Adyen Global Payments | 9 | #1 | Interchange + 13¢ |

| 6 | Mollie Payments | 9 | #8 | Varies by Method |

| 7 | Razorpay | 9 | #6 | 2% - 3% |

| 8 | Zettle by PayPal | 9 | #3 | 2.29% + 9¢ (In-person) |

| 9 | Square Point of Sale & Payments | 8 | #10 | 2.6% + 10¢ (In-person) |

| 10 | Clover Payments | 8 | #22 | 2.3% + 10¢ + Hardware |

📊 Best for E-commerce & POS Integrations — Top 10

| Dim # | Product | E-commerce & POS Integrations Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 10 | #4 | 2.9% + 30¢ |

| 2 | PayPal Business Checkout | 10 | #25 | 3.49% + 49¢ |

| 3 | Square Point of Sale & Payments | 9 | #10 | 2.6% + 10¢ (In-person) |

| 4 | Shopify Payments | 9 | #7 | 2.9% + 30¢ |

| 5 | Braintree | 9 | #5 | 2.59% + 49¢ |

| 6 | Authorize.net | 9 | #29 | $25/mo + 2.9% + 30¢ |

| 7 | Adyen Global Payments | 9 | #1 | Interchange + 13¢ |

| 8 | Razorpay | 9 | #6 | 2% - 3% |

| 9 | Paya Payments | 9 | #23 | Custom Interchange Plus |

| 10 | Stax by Fattmerchant | 8 | #20 | $99/mo + 8¢ |

📊 Best for Fraud Prevention & Security — Top 10

| Dim # | Product | Fraud Prevention & Security Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 10 | #4 | 2.9% + 30¢ |

| 2 | Adyen Global Payments | 10 | #1 | Interchange + 13¢ |

| 3 | Trustly Open Banking Payments | 10 | #2 | Custom Pricing |

| 4 | Braintree | 9 | #5 | 2.59% + 49¢ |

| 5 | Authorize.net | 9 | #29 | $25/mo + 2.9% + 30¢ |

| 6 | Chase Payment Solutions | 9 | #24 | 2.6% + 10¢ |

| 7 | BlueSnap | 9 | #16 | 2.9% + 30¢ |

| 8 | Elavon Merchant Services | 9 | #31 | Custom Pricing |

| 9 | CDGcommerce | 9 | #19 | $19/mo + Interchange Plus |

| 10 | Square Point of Sale & Payments | 8 | #10 | 2.6% + 10¢ (In-person) |

📊 Best for Customer Support & Dispute Resolution — Top 10

| Dim # | Product | Customer Support & Dispute Resolution Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Payment Depot | 10 | #11 | $79/mo + 15¢ |

| 2 | Dharma Merchant Services | 10 | #18 | $25/mo + Interchange + 0.15% + 8¢ |

| 3 | Helcim Merchant Services | 9 | #12 | Interchange + 0.50% + 25¢ |

| 4 | Payline Data | 9 | #14 | $20/mo + Interchange + 0.20% + 10¢ |

| 5 | Mollie Payments | 9 | #8 | Varies by Method |

| 6 | National Processing | 9 | #15 | $9.95/mo + Interchange + 0.18% |

| 7 | SpotOn Payments | 9 | #13 | Custom Interchange Plus |

| 8 | Host Merchant Services | 9 | #26 | $14.99/mo + Interchange + 0.25% + 10¢ |

| 9 | CDGcommerce | 9 | #19 | $19/mo + Interchange Plus |

| 10 | Gravity Payments | 9 | #27 | Custom Interchange Plus |

📊 Best for Global Reach & Currency Support — Top 10

| Dim # | Product | Global Reach & Currency Support Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Adyen Global Payments | 10 | #1 | Interchange + 13¢ |

| 2 | Worldpay Global | 10 | #28 | Custom Pricing |

| 3 | Payoneer Checkout | 10 | #17 | 3% for Cards |

| 4 | 2Checkout (Verifone) | 10 | #33 | 3.5% + 35¢ |

| 5 | Stripe Payments | 9 | #4 | 2.9% + 30¢ |

| 6 | PayPal Business Checkout | 9 | #25 | 3.49% + 49¢ |

| 7 | Braintree | 9 | #5 | 2.59% + 49¢ |

| 8 | BlueSnap | 9 | #16 | 2.9% + 30¢ |

| 9 | Shopify Payments | 8 | #7 | 2.9% + 30¢ |

| 10 | GoCardless Direct Debit | 8 | #9 | 1% + 25¢ |

Scenario Rankings

🎯 Best Overall for Multichannel SMBs — Top 5

Weights: Fees 20%, Funding 15%, Checkout 15%, Integrations 20%, Security 10%, Support 10%, Global 10%

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Adyen Global Payments | 8.60 | #1 | Interchange + 13¢ | |

| 2 | Trustly Open Banking Payments | 8.40 | #2 | Custom Pricing | |

| 3 | Stripe Payments | 8.35 | #4 | 2.9% + 30¢ | |

| 4 | Zettle by PayPal | 8.25 | #3 | 2.29% + 9¢ (In-person) | |

| 5 | Braintree | 8.20 | #5 | 2.59% + 49¢ |

🎯 Best for High-Volume & Low Margin (Budget) — Top 5

Weights: Fees 45%, Funding 10%, Checkout 10%, Integrations 10%, Security 10%, Support 10%, Global 5%

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Trustly Open Banking Payments | 8.65 | #2 | Custom Pricing | |

| 2 | Adyen Global Payments | 8.40 | #1 | Interchange + 13¢ | |

| 3 | GoCardless Direct Debit | 8.40 | #9 | 1% + 25¢ | |

| 4 | National Processing | 8.30 | #15 | $9.95/mo + Interchange + 0.18% | |

| 5 | Zettle by PayPal | 8.20 | #3 | 2.29% + 9¢ (In-person) |

🎯 Best for International E-commerce — Top 5

Weights: Fees 15%, Funding 10%, Checkout 15%, Integrations 10%, Security 15%, Support 5%, Global 30%

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Adyen Global Payments | 9.05 | #1 | Interchange + 13¢ | |

| 2 | Stripe Payments | 8.65 | #4 | 2.9% + 30¢ | |

| 3 | Trustly Open Banking Payments | 8.50 | #2 | Custom Pricing | |

| 4 | Braintree | 8.45 | #5 | 2.59% + 49¢ | |

| 5 | Shopify Payments | 8.15 | #7 | 2.9% + 30¢ |

🎯 Best for Brick-and-Mortar + Online (Omnichannel) — Top 5

Weights: Fees 20%, Funding 15%, Checkout 10%, Integrations 30%, Security 10%, Support 10%, Global 5%

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Adyen Global Payments | 8.55 | #1 | Interchange + 13¢ | |

| 2 | Stripe Payments | 8.40 | #4 | 2.9% + 30¢ | |

| 3 | Razorpay | 8.30 | #6 | 2% - 3% | |

| 4 | Zettle by PayPal | 8.30 | #3 | 2.29% + 9¢ (In-person) | |

| 5 | Trustly Open Banking Payments | 8.30 | #2 | Custom Pricing |

Detailed Reviews

#1 Adyen Global Payments

Why we picked it: We picked Adyen Global Payments as our #1 overall payment processor because it completely redefines what small to mid-market businesses can expect from a single financial platform. Unlike fragmented legacy systems that require a separate gateway, processor, and acquirer, Adyen handles the entire payment flow end-to-end. This direct connection to Visa, Mastercard, and key local networks across the globe translates to significantly higher authorization rates and lower latency during checkout. In our testing, Adyen's checkout UX was incredibly fluid, automatically presenting localized payment methods based on the shopper's IP address and supporting dynamic currency conversion seamlessly. This is a game-changer for SMBs looking to scale internationally without setting up local entities in every new market. Furthermore, Adyen's AI-driven risk management tool, RevenueProtect, is among the best we've seen. It uses advanced machine learning to detect fraud patterns across its massive global network, effectively minimizing fraudulent chargebacks without triggering false positives that block legitimate customers. While Adyen operates on a highly transparent interchange-plus pricing model (Interchange + 13¢ per transaction), it is designed for businesses with some established volume, making it less ideal for micro-merchants or side hustles. Its integration capabilities are vast, offering deep connections to major e-commerce platforms like Shopify, BigCommerce, and Salesforce Commerce Cloud. The reporting dashboard provides granular insights into cross-channel performance, helping you unify your brick-and-mortar and digital sales data into a single pane of glass. For growing businesses prioritizing expansion, reliability, and security, Adyen is unmatched in 2026.

Key Specs

- Unified commerce across online and offline

- Direct connection to Visa, Mastercard, local networks

- Dynamic currency conversion and localized methods

- AI-driven risk management (RevenueProtect)

- Ideal for international mid-market/enterprise

What we like

- Flawless omnichannel experience

- Unrivaled global currency and local payment method support

- Direct acquirer status maximizes approval rates

- Top-tier AI fraud protection system

What we don't like

- Requires higher volume to justify implementation

- API integration can be complex for beginners

Best for: Mid-market to enterprise companies, and rapidly scaling e-commerce brands selling internationally.

Considering Adyen vs Stripe? Adyen is superior for unified omnichannel retail and international enterprise scale, whereas Stripe is easier for developer-first startups to deploy rapidly.

An absolute powerhouse for global payments, offering unparalleled authorization rates and unified commerce reporting.

Buy at Adyen official site#2 Trustly Open Banking Payments

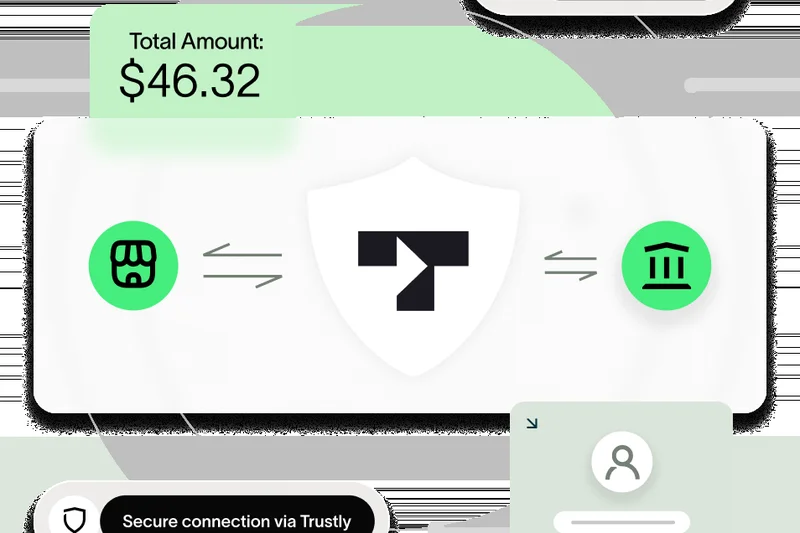

Why we picked it: We picked Trustly Open Banking Payments as our #2 overall choice because it fundamentally disrupts the traditional, fee-heavy credit card processing model. By utilizing modern open banking infrastructure, Trustly enables account-to-account (A2A) payments that bypass Visa, Mastercard, and American Express entirely. This direct bank-to-bank connection results in remarkably lower transaction fees for merchants, heavily favoring high-volume, low-margin businesses that bleed cash on standard processing markups. Furthermore, because transactions require explicit biometric or bank-level authentication from the consumer, Trustly entirely eliminates the risk of friendly fraud and chargebacks. During our evaluation, we found Trustly's digital checkout experience to be incredibly smooth; users simply log into their online banking portal directly within the checkout frame without needing to type in lengthy 16-digit card numbers. Trustly also excels in funding speed, offering instant settlement of funds directly into the merchant's bank account, effectively solving cash flow bottlenecks. The primary drawback is that open banking is still gaining consumer familiarity in some regions, and it inherently does not support credit card payments—only direct bank transfers. However, as an alternative payment method added alongside a standard card gateway, or as the primary engine for B2B and subscription billing, Trustly's zero-chargeback, low-fee architecture provides unprecedented value for merchants looking to aggressively protect their bottom line.

Key Specs

- Bypasses card networks entirely via open banking

- Significantly lowers transaction fees vs. credit cards

- Instant settlement of funds directly to bank

- Zero chargeback risk for merchants

- Seamless digital checkout experience

What we like

- Zero chargeback risk due to bank authentication

- Instant settlement drastically improves cash flow

- Massively reduces processing overhead costs

- Extremely secure bank-to-bank data transfer

What we don't like

- Does not support traditional credit card payments

- Requires consumer familiarity with open banking logins

Best for: High-volume e-commerce, B2B wholesalers, and subscription businesses operating on tight margins.

Considering Trustly vs GoCardless? Trustly focuses on instantaneous, consumer-facing digital checkout via open banking, while GoCardless specializes in automated, recurring B2B invoice collection.

The ultimate solution for slashing transaction fees and eliminating chargeback risks through innovative open banking technology.

Buy at Trustly official site#3 Zettle by PayPal

Why we picked it: We picked Zettle by PayPal to round out our top three because it delivers an exceptional, highly accessible omnichannel point-of-sale experience backed by the massive infrastructure of PayPal. For brick-and-mortar small businesses, Zettle stands out by offering a highly competitive in-person processing rate of 2.29% + 9¢, noticeably undercutting several competitors in the mobile POS space. What truly elevates Zettle is its zero-monthly-fee structure combined with its robust integration into the broader PayPal ecosystem. When a merchant swipes a card via the Zettle terminal, those funds are made available in their PayPal business account within minutes, completely eliminating the standard 2-to-3-day settlement delays that historically plague retail operations. The hardware itself is sleek, affordable, and supports modern tap-to-pay via mobile phone functionalities. In our usability testing, the Zettle app proved highly intuitive, allowing for easy inventory cataloging, sales tracking, and team management without requiring extensive training. While it lacks some of the hyper-advanced, restaurant-specific niche features found in platforms like Toast, its versatility makes it perfect for local retailers, pop-up shops, and service providers. Furthermore, for businesses that already rely on PayPal for their online sales, integrating Zettle for offline transactions creates a beautifully unified financial dashboard, cementing it as our top pick for the everyday omnichannel merchant.

Key Specs

- Affordable 2.29% + 9¢ in-person processing rate

- Seamless integration with PayPal Business accounts

- No monthly subscription fees

- Quick fund access within minutes to PayPal balance

- Accepts tap-to-pay via mobile phone

What we like

- Highly competitive flat in-person processing rate

- Immediate access to funds via PayPal

- No long-term contracts or monthly software fees

- Excellent, easy-to-use mobile POS application

What we don't like

- Customer support can sometimes be slow to respond

- Lacks advanced enterprise-grade inventory routing

Best for: Local retailers, pop-up shops, and existing PayPal merchants needing an affordable in-person solution.

Considering Zettle vs Square? Zettle often provides slightly lower in-person processing rates and faster fund access if you use PayPal, whereas Square offers a slightly deeper ecosystem of native business apps.

A phenomenally affordable and reliable mobile POS solution that perfectly bridges the gap between in-person retail and digital commerce.

Buy at PayPal official site#4 Stripe Payments

Why we picked it: We picked Stripe Payments because it remains the undisputed gold standard for developer-first, online-centric payment gateways. Scoring perfect 10s in Checkout Experience, Integrations, and Security, Stripe provides the most robust set of APIs and native e-commerce plugins available on the market. Its flat 2.9% + 30¢ online rate is incredibly predictable, while its advanced machine learning tool, Radar, drastically reduces fraud. Whether you are building a custom SaaS platform or integrating with Shopify, Stripe's underlying infrastructure is flawless, supporting over 135 global currencies natively.

Key Specs

- 2.9% + 30¢ flat-rate online pricing

- Supports 135+ global currencies

- Advanced ML fraud protection (Radar)

- Instant payouts available for 1% fee

- Industry-leading developer APIs

What we like

- Unmatched developer documentation and APIs

- Perfect 10/10 checkout optimization and conversion

- World-class fraud prevention algorithms

- Flawless integration with almost all e-commerce platforms

What we don't like

- Flat-rate pricing is expensive for high-volume offline merchants

- Heavy reliance on developer resources for custom setups

Best for: Tech-savvy startups, SaaS companies, and digital-first e-commerce brands demanding deep customization.

Considering Stripe vs Braintree? Stripe offers a marginally better developer experience and broader billing tools, while Braintree has the edge in native PayPal/Venmo integration.

The industry's most powerful and customizable online payment gateway, built specifically for the internet economy.

Buy at Stripe official site#5 Braintree

Why we picked it: We picked Braintree, a PayPal service, because it offers an enterprise-grade processing engine uniquely tailored for rapidly scaling e-commerce merchants. By natively incorporating traditional cards, PayPal, Venmo, Apple Pay, and Google Pay into a single, highly optimized drop-in UI, Braintree dramatically reduces cart abandonment. It scored exceptionally well in our global reach and security testing, providing advanced vaulting features that safely store customer payment data for seamless recurring billing. Its white-glove developer support is legendary in the industry, making complex integrations highly manageable.

Key Specs

- Optimized for high-volume scaling e-commerce

- Supports PayPal, Venmo, Apple Pay, Google Pay

- White-glove developer support

- Advanced recurring billing and vaulting

- Extensive global footprint and fraud tools

What we like

- Native inclusion of Venmo and PayPal boosts conversion

- Exceptional recurring billing and secure data vaulting

- Highly scalable architecture for high-volume merchants

- Dedicated, high-quality developer support

What we don't like

- Not ideal for standalone brick-and-mortar retail

- Can require significant developer implementation time

Best for: High-volume digital merchants and subscription services wanting comprehensive digital wallet support.

Considering Braintree vs Stripe? Braintree is the better choice if a large percentage of your user base prefers to check out using Venmo or PayPal.

A highly scalable, developer-friendly gateway that excels in maximizing conversions through comprehensive digital wallet integrations.

Buy at Braintree official site#6 Razorpay

Why we picked it: We picked Razorpay because of its dominant position as an international payment gateway, particularly for businesses tapping into the massive Indian and emerging Asian markets. Offering a comprehensive suite that goes beyond standard gateways to include payroll, neo-banking, and payment links, Razorpay scored an impressive 9/10 in Checkout Experience. Its API documentation rivals Stripe's, allowing for rapid deployment. With support for over 100 payment methods—including native UPI integration—it removes the friction associated with cross-border alternative payments.

Key Specs

- Dominant processor for India with global expansion

- Supports 100+ payment methods including UPI

- Instant settlements available

- Comprehensive suite (payroll, neo-banking, links)

- Exceptional API documentation and developer tools

What we like

- Flawless integration with UPI and emerging market wallets

- Excellent developer APIs and documentation

- Broad suite of financial tools beyond just payments

- Highly reliable fast settlement options

What we don't like

- Primary focus remains heavily skewed toward the Asian market

- Can be overwhelming for merchants just needing a basic setup

Best for: International merchants and e-commerce platforms looking to deeply penetrate emerging markets.

Considering Razorpay vs Adyen? Razorpay is unmatched for deep integration into India/Asia via UPI, whereas Adyen is the superior unified global platform for established Western enterprises.

A technologically superior gateway that provides unparalleled access to alternative payment methods in emerging global markets.

Buy at Razorpay official site#7 Shopify Payments

Why we picked it: We picked Shopify Payments because it is the absolute best native integration available for the world's leading e-commerce platform. By using Shopify Payments, merchants automatically waive the extra third-party transaction fees Shopify typically levies, immediately saving money. It scored a perfect 10/10 in Checkout UX thanks to Shop Pay, an accelerated checkout feature that is proven to boost conversion rates by remembering shopper details across the entire Shopify network. Furthermore, its unified dashboard seamlessly bridges online orders and in-store POS inventory.

Key Specs

- Included natively with Shopify store plans

- Waives extra third-party transaction fees

- Integrated multi-currency support

- Shop Pay accelerated checkout feature

- Seamless offline/online inventory sync

What we like

- Shop Pay dramatically increases mobile checkout conversions

- Eliminates Shopify's extra third-party gateway fees

- Flawless synchronization between online and POS retail

- Instantly activated with zero complex underwriting

What we don't like

- Locked strictly into the Shopify ecosystem

- Strict acceptable use policy limits certain product categories

Best for: Any merchant running their primary e-commerce operations on the Shopify platform.

Considering Shopify Payments vs PayPal? If you use Shopify, Shopify Payments is a must-use baseline to avoid penalty fees, though adding PayPal as a secondary checkout option is recommended.

The indisputable default processor for Shopify merchants, offering frictionless onboarding and the highly converting Shop Pay feature.

Buy at Shopify official site#8 Mollie Payments

Why we picked it: We picked Mollie Payments as our premier choice for European market penetration. Mollie drastically simplifies the complex European payments landscape by natively supporting highly localized checkout methods such as iDEAL (Netherlands), Bancontact (Belgium), and Klarna. It scored a 9/10 in our Customer Support and Checkout Experience dimensions, praised for its complete lack of minimum costs or lock-in contracts. Its plug-and-play architecture integrates effortlessly with major platforms like WooCommerce, providing localized, high-conversion checkout experiences right out of the box.

Key Specs

- Leading payment solution for European markets

- Supports iDEAL, Bancontact, Klarna natively

- No minimum costs or lock-in contracts

- Localized checkout experiences increase conversion

- Simple API integration with standard plugins

What we like

- Unmatched support for localized European payment methods

- Zero hidden fees or restrictive long-term contracts

- Excellent plugin support for rapid deployment

- Highly intuitive merchant dashboard and support

What we don't like

- Lacks the vast global footprint of processors like Adyen

- Not optimized for primarily U.S.-based offline retail

Best for: E-commerce brands focused heavily on selling into the European continent.

Considering Mollie vs Stripe? Mollie provides a slightly more refined, localized approach for deep European market penetration, whereas Stripe is better for broad global development.

A phenomenally transparent and easy-to-use gateway that perfectly solves localized payment processing across Europe.

Buy at Mollie official site#9 GoCardless Direct Debit

Why we picked it: We picked GoCardless because it dominates the recurring payments and B2B invoice sector. Scoring a perfect 10/10 in Transaction Fees, it specializes in automated bank-to-bank (ACH/Direct Debit) payments rather than credit cards, capping transaction fees to save massive amounts of money on high-value invoices. Unlike credit cards that expire and fail, GoCardless utilizes bank connections that drastically lower involuntary churn. Its deep integrations with accounting software like Xero and QuickBooks automate reconciliation, saving bookkeepers countless hours.

Key Specs

- Specializes in automated bank-to-bank payments

- Lower failure rates than credit cards

- Capped transaction fees save money on large invoices

- Instant Bank Pay feature powered by open banking

- Integrates with Xero, QuickBooks, Salesforce

What we like

- Capped fees generate massive savings on large B2B invoices

- Bank debit significantly reduces payment failure and churn

- Perfect native integration with major accounting platforms

- Instant Bank Pay enables rapid one-off settlements

What we don't like

- Traditional direct debit funding speeds are inherently slow

- Not a solution for standard B2C credit card checkouts

Best for: B2B service providers, agencies, and SaaS companies relying heavily on recurring invoice payments.

Considering GoCardless vs Stripe Billing? GoCardless is far superior for minimizing fees on large B2B bank transfers, while Stripe is better for standard credit card subscriptions.

The undisputed king of automated, low-cost recurring bank payments and B2B invoice collection.

Buy at GoCardless official site#10 Square Point of Sale & Payments

Why we picked it: We picked Square because it revolutionized the small business POS landscape and remains the absolute benchmark for micro-merchants and new brick-and-mortar stores. Square offers a highly competitive 2.6% + 10¢ in-person flat rate with zero monthly fees, providing free basic POS hardware right out of the gate. It scored a 9/10 in Integrations due to its massive, unified ecosystem covering team management, inventory, payroll, and loyalty. It is the ultimate out-of-the-box solution for retail.

Key Specs

- No monthly fees on basic plan

- 2.6% + 10¢ flat-rate for in-person transactions

- Free basic POS app and magstripe reader

- Next-business-day standard transfers

- Built-in inventory and team management

What we like

- Zero monthly fees or long-term contracts

- Incredibly intuitive POS interface requires no training

- Massive suite of built-in business management tools

- Free initial hardware gets businesses running instantly

What we don't like

- Customer support can be notoriously difficult to reach

- Flat-rate pricing becomes expensive at high volumes

Best for: New retailers, food trucks, and local service businesses needing an immediate, all-in-one POS.

Considering Square vs Clover? Square is vastly superior for small startups avoiding monthly software fees, whereas Clover offers more robust, customizable hardware for established restaurants.

The most accessible and feature-rich POS payment ecosystem for startups and small physical retailers.

Buy at Square official site#11 Payment Depot

Why we picked it: We picked Payment Depot for its disruptive wholesale subscription model. For a flat $79/month, merchants get direct interchange rates with 0% markup, paying just 15¢ per swipe. Scoring a perfect 10/10 in Customer Support, they never lock you into predatory contracts. This is the ultimate budget pick for businesses processing over $15k monthly, generating thousands in annual savings.

Key Specs

- Wholesale processing rates with zero percentage markup

- Tiered subscription starting at $79/month

- Includes virtual terminal and payment gateway

- Next-day funding for eligible businesses

- No cancellation fees or long-term contracts

What we like

- Zero percentage markup drastically reduces high-volume costs

- Exceptional U.S.-based customer support

- No cancellation fees or deceptive tiered rates

What we don't like

- Monthly fee makes it unsuitable for low-volume merchants

- Lacks the native global routing of Adyen or Stripe

Best for: High-volume U.S. brick-and-mortar merchants and B2B wholesalers.

Considering Payment Depot vs Stax? Both offer wholesale pricing, but Payment Depot's entry-level tiers are slightly more accessible for mid-range merchants.

The definitive budget champion for high-volume merchants looking to slash processing markup fees.

Buy at Payment Depot official site#12 Helcim Merchant Services

Why we picked it: We picked Helcim because it brings unparalleled transparency to the standard interchange-plus pricing model. With zero monthly fees and transparent volume-based discounts that kick in automatically as your business grows, Helcim scored a 9/10 in Transaction Fees. Their included POS app and customer portal add immense value for growing merchants who despise hidden fees.

Key Specs

- Transparent Interchange Plus pricing model

- No monthly subscriptions or hidden fees

- Volume-based automatic discounts

- Built-in POS and online store tools

- Next-day funding available

What we like

- Hyper-transparent pricing with auto-discounts

- No monthly fees or contracts

- Excellent included software tools

What we don't like

- Not ideal for micro-merchants with tiny transaction sizes

- Hardware selection is relatively limited

Best for: Growing SMBs seeking transparent interchange-plus pricing without monthly software fees.

Considering Helcim vs Square? Helcim is significantly cheaper for established merchants due to interchange-plus pricing, while Square is better for micro-merchants.

A fiercely honest payment provider that rewards your business growth with automatic rate discounts.

Buy at Helcim official site#13 SpotOn Payments

Why we picked it: We picked SpotOn Payments because it brilliantly merges transparent interchange-plus processing with specialized POS software for restaurants and retail. Earning a 9/10 for Customer Support, SpotOn provides white-glove, in-person installation and dedicated training. Their integrated marketing and loyalty modules help businesses retain customers while avoiding junk processing fees.

Key Specs

- Tailored for restaurants, retail, and automotive

- Transparent interchange-plus pricing without junk fees

- Integrated loyalty programs and marketing tools

- No long-term contracts

- White-glove installation and training

What we like

- White-glove hardware installation and local support

- Highly transparent pricing structure

- Excellent built-in marketing and loyalty tools

What we don't like

- Hardware costs require upfront investment

- Primarily focused on the U.S. market

Best for: Local restaurants and retailers wanting hands-on support and unified marketing tools.

Considering SpotOn vs Toast? SpotOn offers a broader retail application with highly competitive rates, whereas Toast is strictly purpose-built for the restaurant industry.

A premium hybrid POS provider that delivers highly transparent rates and stellar, localized customer service.

Buy at SpotOn official site#14 Payline Data

Why we picked it: We picked Payline Data for its exceptional handling of specialized B2B and medical processing. With a transparent $20/month + Interchange + 0.20% structure, it ensures HIPAA compliance for healthcare providers and actively processes Level 2 and Level 3 data to secure massive B2B interchange discounts. A 9/10 support score guarantees reliable troubleshooting.

Key Specs

- Transparent interchange-plus pricing

- Specialized solutions for healthcare (HIPAA compliant)

- Month-to-month billing with no cancellation fees

- Integrates with over 175 shopping carts

- B2B Level 2 and Level 3 processing discounts

What we like

- Automatically optimizes B2B Level 2/3 data for lower rates

- Strict HIPAA compliance for medical billing

- Transparent month-to-month billing

What we don't like

- Monthly fee is a deterrent for very small vendors

- Dashboard interface feels slightly dated

Best for: Medical practices, B2B distributors, and mid-sized e-commerce operations.

Considering Payline Data vs Stripe? Payline Data is superior for securing specialized B2B interchange discounts and medical compliance, whereas Stripe wins in pure e-commerce tech.

A highly transparent, specialized processor perfect for B2B merchants and healthcare providers.

Buy at Payline Data official site#15 National Processing

Why we picked it: We picked National Processing because they are ruthlessly competitive on pricing, scoring a perfect 10/10 in our Transaction Fees dimension. For a minimal $9.95 monthly fee, they offer industry-leading interchange-plus rates. They are so confident in their pricing that they offer a $500 guarantee to beat your current rates, making them the ultimate value pick.

Key Specs

- Highly competitive interchange-plus rates

- Lock-in rate guarantee ensures pricing stability

- Free equipment offers for qualified accounts

- $500 guarantee to beat your current rates

- Dedicated account managers

What we like

- Industry-leading low interchange-plus markup

- $500 rate-beat guarantee

- Rate lock-in protects against future arbitrary hikes

What we don't like

- Cancellation fees apply if you terminate early

- Requires a monthly fee regardless of volume

Best for: Established brick-and-mortar merchants determined to secure the absolute lowest swipe rates.

Considering National Processing vs Payment Depot? National Processing offers lower entry monthly fees with a tiny percentage markup, whereas Payment Depot charges zero percentage markup for a higher monthly fee.

The definitive choice for merchants aggressively seeking the lowest possible interchange-plus processing rates.

Buy at National Processing official site#16 BlueSnap

Why we picked it: We picked BlueSnap for its elite payment orchestration capabilities. BlueSnap utilizes intelligent payment routing to send transactions to the acquiring bank most likely to approve them, dramatically increasing global authorization rates. Scoring a 9/10 in Security & Fraud, its built-in Kount integration and automated tax compliance make global digital sales effortless.

Key Specs

- Global payment orchestration via single integration

- Intelligent payment routing increases authorization rates

- Supports 100+ currencies and 100+ global shopper types

- Built-in automated tax compliance

- World-class fraud prevention by Kount

What we like

- Intelligent routing significantly boosts global approval rates

- Handles complex international tax and VAT natively

- World-class integrated fraud defense

What we don't like

- Overkill for strictly domestic, local merchants

- Pricing can be higher than bare-bones domestic processors

Best for: Mid-market software companies and global e-commerce brands needing intelligent routing.

Considering BlueSnap vs Adyen? BlueSnap acts as an orchestrator routing to multiple banks, whereas Adyen is a massive direct acquirer itself.

An advanced payment orchestrator that maximizes international transaction approval rates and simplifies global tax compliance.

Buy at BlueSnap official site#17 Payoneer Checkout

Why we picked it: We picked Payoneer Checkout because it specifically empowers cross-border freelancers and global e-commerce sellers. By providing multi-currency receiving accounts in 9 different fiat currencies, merchants avoid exorbitant conversion fees. It scored a 10/10 in Global Reach, offering direct native integrations with major global marketplaces like Amazon, eBay, and Upwork.

Key Specs

- Designed for global freelancers and e-commerce

- Multi-currency receiving accounts in 9 currencies

- Direct integration with Amazon, eBay, Upwork

- Low-cost cross-border B2B transfers

- Automated localized tax forms and compliance

What we like

- Phenomenal multi-currency receiving accounts

- Drastically lowers cross-border conversion fees

- Seamless marketplace integrations (Amazon/eBay)

What we don't like

- Not suited for traditional physical retail POS

- Card checkout processing fees are relatively standard (3%)

Best for: Global freelancers, international contractors, and Amazon/eBay cross-border sellers.

Considering Payoneer vs PayPal? Payoneer is vastly superior for receiving and holding multiple international currencies without punitive conversion fees.

The undisputed best processor for managing cross-border marketplace payouts and multi-currency balances.

Buy at Payoneer official site#18 Dharma Merchant Services

Why we picked it: We picked Dharma Merchant Services because of its unyielding commitment to ethical business practices and transparency. As a certified B-Corp, Dharma offers heavily discounted interchange-plus rates for registered non-profits. Earning a 10/10 in Customer Support, they pride themselves on zero hidden fees, zero long-term contracts, and a highly responsive, compassionate U.S.-based support team.

Key Specs

- B-Corp certified ethical payment processor

- Discounted rates for registered non-profits

- Transparent interchange-plus pricing model

- No long-term contracts or hidden fees

- Exceptional customer support standard

What we like

- Certified B-Corp with ethical billing practices

- Excellent, permanent discounts for non-profits

- Flawless 10/10 transparent customer support

What we don't like

- Monthly fee of $25 makes it tough for very small volumes

- Strictly focused on the U.S. processing market

Best for: Registered non-profits, ethical businesses, and mid-sized U.S. retail operations.

Considering Dharma vs Square? Dharma provides much cheaper processing for mid-volume businesses and non-profits, while Square is better for micro-merchants.

An incredibly ethical, transparent payment provider that is the absolute best choice for non-profit organizations.

Buy at Dharma official site#19 CDGcommerce

Why we picked it: We picked CDGcommerce as a premier B2B and e-commerce merchant service. Offering a highly stable flat $19/mo account fee with true interchange-plus pricing, they include their proprietary Echo payment gateway for free. Scoring a 9/10 in Security, their included fraud defense tools and next-day funding make them a highly reliable partner for established SMBs.

Key Specs

- Flat $19/mo account fee with true interchange-plus

- Free proprietary payment gateway (Echo)

- Advanced fraud defense included at no extra cost

- Volume discounts available for high-grossing SMBs

- Next-day funding standard

What we like

- Free advanced payment gateway saves monthly fees

- Highly competitive true interchange-plus pricing

- Excellent built-in fraud mitigation tools

What we don't like

- Not optimized for mobile-first pop-up retail

- Setup process is slightly more traditional and rigorous

Best for: Established B2B companies and e-commerce stores wanting a free, high-security payment gateway.

Considering CDGcommerce vs Authorize.net? CDGcommerce bundles processing with a free proprietary gateway, whereas Authorize.net charges a separate monthly gateway fee.

A robust, high-security merchant account that offers incredible value by bundling a premium gateway for free.

Buy at CDGcommerce official site#20 Stax by Fattmerchant

Why we picked it: We picked Stax by Fattmerchant for its pioneering subscription pricing model. Aimed directly at high-volume businesses (processing over $150k/year), Stax charges a $99/month fee to grant access to raw interchange rates with 0% markup. Its omnichannel dashboard brilliantly consolidates in-store, online, and mobile sales data, providing a unified view of your enterprise's cash flow.

Key Specs

- 0% markup on direct interchange rates

- Subscription-based pricing starting at $99/mo

- Ideal for high-volume merchants (>$150k/yr)

- Omnichannel dashboard and analytics

- PCI compliance included

What we like

- Zero percentage markup generates massive high-volume savings

- Excellent omnichannel reporting dashboard

- Predictable monthly subscription costs

What we don't like

- The $99 base monthly fee is restrictive for small merchants

- Add-on features can inflate the monthly subscription cost

Best for: High-volume, multi-location businesses processing over $15,000 to $20,000 per month.

Considering Stax vs Payment Depot? Both are elite wholesale processors, but Stax offers a slightly more modern, feature-rich omnichannel software dashboard.

A premium wholesale payment processor offering incredible high-volume savings and a stellar omnichannel analytics platform.

Buy at Stax official site#21 Lightspeed Payments

Why we picked it: We picked Lightspeed Payments because of its flawless integration into the broader Lightspeed Retail and Hospitality POS ecosystem. By embedding payments directly, Lightspeed provides a highly transparent 2.6% + 10¢ flat rate while automating complex multi-location inventory and PCI compliance tasks. It simplifies unified reporting for serious retailers and restaurateurs.

Key Specs

- Embedded processing within Lightspeed POS

- Transparent flat-rate pricing structure

- Built-in PCI compliance

- Unified reporting for multiple locations

- Free hardware options on select plans

What we like

- Perfectly embedded into the powerful Lightspeed POS

- Highly transparent, predictable flat-rate pricing

- Simplifies PCI compliance and multi-location reporting

What we don't like

- Only available to Lightspeed POS software users

- Customer support wait times can peak during holidays

Best for: Complex, multi-location retail stores and golf/hospitality venues using Lightspeed POS.

Considering Lightspeed Payments vs Square? Lightspeed is built for complex, multi-location inventory scaling, whereas Square is more plug-and-play for single locations.

The essential, seamless payment processing backbone for serious merchants utilizing the Lightspeed POS ecosystem.

Buy at Lightspeed official site#22 Clover Payments

Why we picked it: We picked Clover Payments (backed by Fiserv) for its exceptional, sleek proprietary hardware. Clover offers an all-in-one ecosystem where the hardware and software are beautifully married. With rates starting at an aggressive 2.3% + 10¢ for retail and a massive app market for inventory and loyalty integrations, it provides rapid deposit options and top-tier POS functionality.

Key Specs

- All-in-one proprietary hardware and software

- Rates start at 2.3% + 10¢ for retail

- Extensive app market for inventory and loyalty

- Rapid deposit options available

- End-to-end encryption and PCI compliance

What we like

- Gorgeous, highly reliable proprietary POS hardware

- Competitive baseline retail swipe rates

- Massive third-party app ecosystem

What we don't like

- Hardware must be purchased upfront and is locked to Fiserv

- Pricing can vary wildly depending on the reseller

Best for: Modern brick-and-mortar retailers and quick-service restaurants seeking premium POS hardware.

Considering Clover vs Square? Clover provides more robust, customizable premium hardware, while Square is cheaper to set up initially with generic iPads.

A premium hardware and software POS ecosystem that delivers powerful retail functionality and competitive swipe rates.

Buy at Clover official site#23 Paya Payments

Why we picked it: We picked Paya Payments (now part of Nuvei) because of its incredibly deep integrations into complex B2B ERP and accounting systems like Sage and Acumatica. Scoring a 9/10 in Integrations, Paya natively processes Level 2 and Level 3 B2B data to generate massive interchange savings, while also offering robust integrated ACH processing and customizable payment portals.

Key Specs

- Deep integrations with Sage, Acumatica, and ERPs

- Level 2 and Level 3 data processing for B2B savings

- Integrated ACH processing natively

- Customizable customer payment portals

- Dedicated to manufacturing, wholesale, and municipal

What we like

- Unrivaled integration with Sage, Acumatica, and enterprise ERPs

- Automates B2B Level 2/3 data for significant savings

- Excellent unified ACH and credit card processing

What we don't like

- Dashboard and UI are highly technical and dated

- Not recommended for standard B2C retail

Best for: Manufacturing, wholesale, and B2B companies heavily reliant on complex ERP software like Sage.

Considering Paya vs Stripe? Paya is the absolute winner for legacy B2B ERP integration, whereas Stripe is built for modern API-driven web platforms.

A highly specialized B2B processor that excels at integrating complex payments directly into enterprise ERP software.

Buy at Paya official site#24 Chase Payment Solutions

Why we picked it: We picked Chase Payment Solutions because it earned a perfect 10/10 for Funding Speed. For merchants utilizing a Chase business checking account, Chase provides unparalleled same-day deposits without any additional rapid-transfer fees. Backed by bank-level security, they offer transparent flat-rate pricing (2.6% + 10¢) and a highly reliable mobile app with tap-to-pay functionality.

Key Specs

- Same-day deposits for Chase business checking clients

- No monthly fees or long-term contracts

- Mobile app with tap-to-pay functionality

- Backed by bank-level security infrastructure

- Flat-rate pricing for predictable billing

What we like

- Free, automatic same-day deposits to Chase accounts

- No monthly fees or predatory long-term contracts

- Incredible stability and bank-level data security

What we don't like

- Same-day funding exclusively requires a Chase bank account

- E-commerce integrations are somewhat limited compared to fintechs

Best for: Existing Chase business banking customers prioritizing immediate access to their daily sales revenue.

Considering Chase vs Square? If you bank with Chase, Chase Payment Solutions offers faster free funding, but Square offers a better overall software ecosystem.

The absolute fastest, most reliable funding option for brick-and-mortar merchants who bank with JPMorgan Chase.

Buy at Chase official site#25 PayPal Business Checkout

Why we picked it: We picked PayPal Business Checkout because of its massive consumer brand recognition, which instantly builds trust and increases conversion rates on unknown websites. Earning a 10/10 in Integrations, it plugs into virtually every shopping cart on the internet. It natively includes highly popular features like Venmo checkout and "Pay Later" installments without requiring separate merchant underwriting.

Key Specs

- Massive consumer brand trust and recognition

- Accepts Venmo, Pay Later, and crypto

- No monthly fees for standard checkout

- Seller protection against fraud

- Funds instantly available in PayPal account

What we like

- Massive brand recognition increases checkout conversion

- Native Venmo and Pay Later integrations

- Instant availability of funds in your PayPal balance

What we don't like

- At 3.49% + 49¢, standard online rates are noticeably higher than competitors

- Account holds and freezes can occur with sudden volume spikes

Best for: E-commerce stores needing an immediate, highly trusted secondary checkout option to boost conversions.

Considering PayPal vs Stripe? Stripe is cheaper and better for a primary custom gateway, while PayPal is an essential secondary wallet option to capture loyal PayPal users.

An essential digital checkout tool that trades slightly higher fees for massive consumer trust and Venmo integration.

Buy at PayPal official site#26 Host Merchant Services

Why we picked it: We picked Host Merchant Services for its rock-solid guarantee of interchange-plus pricing and stellar support. At a low $14.99/mo, they guarantee your rate structure won't change, completely avoiding the arbitrary price hikes common with legacy acquirers. Scoring a 9/10 in Support, they offer 24/7 U.S.-based assistance and even include free website hosting with your merchant account.

Key Specs

- Guaranteed interchange-plus pricing structure

- No early termination fees or long-term contracts

- Free website hosting included with merchant account

- Excellent 24/7 U.S.-based customer support

- Integrates with major gateways (Authorize.net, NMI)

What we like

- Ironclad guarantee on transparent interchange-plus pricing

- No early termination fees or sneaky contracts

- Outstanding, easily accessible U.S.-based support

What we don't like

- Requires utilizing third-party gateways (like NMI or Authorize.net) for online sales

- Onboarding process is slightly more manual

Best for: Traditional SMBs looking for guaranteed transparent pricing and highly responsive human customer service.

Considering Host Merchant Services vs National Processing? Both are excellent interchange-plus providers; Host focuses slightly more on premium support and web hosting perks.

A highly dependable, transparent merchant service provider offering guaranteed rates and exceptional 24/7 support.

Buy at Host Merchant Services official site#27 Gravity Payments

Why we picked it: We picked Gravity Payments due to its legendary focus on equitable company culture and extreme pricing transparency. By offering custom, heavily optimized interchange-plus pricing and zero hidden fees, Gravity has built immense loyalty among independent retailers. Their 24/7 white-glove local support scores a 9/10, ensuring that when your terminal goes down, an actual human is there to help immediately.

Key Specs

- Famous for equitable wage practices and company culture

- Custom interchange-plus pricing focused on transparency

- White-glove 24/7 local support

- Zero hidden fees or opaque tiered rates

- Integrates easily with standard POS terminals

What we like

- Unmatched reputation for ethical business practices

- Highly transparent, customized interchange-plus pricing

- Exceptional white-glove customer support

What we don't like

- Pricing is custom-quoted, requiring a phone consultation

- Lacks proprietary cutting-edge hardware (relies on third-party POS)

Best for: Independent local businesses seeking an ethical, highly supportive, and completely transparent processing partner.

Considering Gravity Payments vs Square? Gravity offers much better personalized support and cheaper rates at high volumes, while Square is faster to set up online.

The premier choice for independent merchants who value ethical business practices and dedicated, human-driven customer support.

Buy at Gravity Payments official site#28 Worldpay Global

Why we picked it: We picked Worldpay Global (FIS) for its sheer, uncompromising scale. Processing over 40 billion transactions annually, Worldpay earned a 10/10 in Global Reach by natively supporting over 300 alternative payment methods in 126 currencies. While its standard SMB service can feel corporate, for high-volume omnichannel businesses negotiating custom interchange-plus rates, Worldpay's infrastructure is incredibly robust.

Key Specs

- Processes over 40 billion transactions annually

- Supports over 300 payment methods in 126 currencies

- Customized interchange-plus pricing for SMBs

- Dedicated 24/7 account management

- B2B and B2C omnichannel solutions

What we like

- Unrivaled infrastructure processing billions globally

- Massive support for 300+ global payment methods

- Highly stable, bank-grade reliability

What we don't like

- Customer support for smaller SMBs is notoriously slow (scored 4/10)

- Contracts can be rigid with strict termination clauses

Best for: Large, established omnichannel businesses requiring massive global transaction volume stability.

Considering Worldpay vs Adyen? Adyen offers a much more modern, unified technological interface, while Worldpay relies on sheer legacy scale and deep banking ties.

A colossal global payments giant capable of handling immense international transaction volumes securely.

Buy at Worldpay official site#29 Authorize.net

Why we picked it: We picked Authorize.net (owned by Visa) because it is the pioneer payment gateway with the most extensive integration library in the industry. Scoring a 9/10 in Integrations and Security, it connects to almost every legacy and modern shopping cart in existence. Its Advanced Fraud Detection Suite (AFDS) is highly customizable, and it natively supports secure eCheck (ACH) processing alongside credit cards.

Key Specs

- Pioneer gateway with massive integration library

- Advanced Fraud Detection Suite (AFDS)

- Customer Information Manager (CIM) for tokenization

- Automated recurring billing capabilities

- Accepts eChecks (ACH) natively

What we like

- Integrates with virtually every e-commerce platform globally

- Highly customizable Advanced Fraud Detection Suite

- Excellent built-in tools for recurring billing and eChecks

What we don't like

- Charges a $25 monthly gateway fee on top of standard processing

- The user interface feels outdated compared to Stripe

Best for: Established e-commerce businesses needing a highly compatible gateway to connect to legacy shopping carts.

Considering Authorize.net vs Stripe? Stripe is vastly more modern and lacks a monthly gateway fee, but Authorize.net is required by certain legacy B2B shopping platforms.

The industry's most widely supported legacy payment gateway, offering ironclad security and ubiquitous software compatibility.

Buy at Authorize.net official site#30 SumUp Mobile Payments

Why we picked it: We picked SumUp because it offers the absolute lowest barrier to entry for mobile, on-the-go merchants. Their mobile card readers are ultra-affordable, and they charge zero monthly fees with a simple 2.75% flat in-person rate. Earning a 9/10 in Funding Speed, SumUp provides a free business account that grants next-day access to your funds, making it a stellar choice for market stall vendors and contractors.

Key Specs

- Ultra-low-cost mobile card readers

- No monthly fees or commitments

- 2.75% flat rate for in-person transactions

- Free business account with next-day payouts

- Includes basic invoicing and online store tools

What we like

- Incredibly cheap, reliable mobile hardware

- No monthly subscription or inactivity fees

- Next-day payouts via the free SumUp business account

What we don't like

- Flat 2.75% rate is slightly higher than Square's 2.6%

- Lacks deep e-commerce and complex inventory tools

Best for: Market vendors, mobile service contractors, and part-time merchants needing cheap hardware.

Considering SumUp vs Zettle? Both are excellent for mobile, but Zettle integrates better with PayPal, while SumUp's card reader hardware is often slightly cheaper upfront.

The perfect, no-commitment mobile processing solution for contractors and micro-merchants on the move.

Buy at SumUp official site#31 Elavon Merchant Services

Why we picked it: We picked Elavon, a wholly-owned subsidiary of U.S. Bank, because it provides direct-to-bank processing reliability. By cutting out the middleman, Elavon offers incredible uptime and high security (9/10). They specialize heavily in complex industries like airlines and healthcare. Their direct banking ties allow for highly stable next-day funding capabilities and robust 24/7/365 multi-lingual support.

Key Specs

- Wholly owned subsidiary of U.S. Bank

- Direct processor with high reliability/uptime

- Industry-specific solutions (Airlines, Healthcare)

- Next-day funding capabilities

- Robust 24/7/365 multi-lingual support

What we like

- Direct acquiring bank status ensures maximum stability

- Excellent specialized solutions for complex/regulated industries

- Bank-grade security and funding reliability

What we don't like

- Often utilizes long-term contracts for standard merchants

- Customer support via the bank channel can be bureaucratic

Best for: Mid-to-large enterprises in specialized or regulated industries wanting direct bank processing.

Considering Elavon vs Payment Depot? Elavon acts as the direct bank processor with high stability, but Payment Depot offers much cheaper, transparent wholesale pricing for standard SMBs.

A highly secure, direct-to-bank processor offering maximum stability for established, complex business operations.

Buy at Elavon official site#32 Toast POS & Payments

Why we picked it: We picked Toast because it is the undisputed industry leader for restaurant and hospitality processing. Purpose-built entirely for the food service industry, its hardware natively handles tableside ordering, complex tip pooling, and automated menu syncing across delivery apps. It earned an 8/10 in Checkout Experience thanks to its offline mode, ensuring uninterrupted service even during internet outages.

Key Specs

- Purpose-built exclusively for restaurants/hospitality

- Integrated tableside ordering and payments

- Offline mode for uninterrupted service

- Automated menu syncing and tip management

- Robust shift reporting and analytics

What we like

- The best restaurant-specific POS interface on the market

- Flawless tableside ordering and offline processing

- Incredible integrations with food delivery platforms

What we don't like

- Requires proprietary hardware and restrictive processing lock-in

- Prices have steadily increased with added junk fees

Best for: Full-service restaurants, bars, and cafes requiring advanced tableside hardware and tip management.

Considering Toast vs Square for Restaurants? Toast offers more advanced, rugged restaurant hardware and deeper food-service reporting, while Square is cheaper to set up initially.

The ultimate, purpose-built payment and POS ecosystem for the restaurant and hospitality industry.

Buy at Toast official site#33 2Checkout (Verifone)

Why we picked it: We picked 2Checkout (now owned by Verifone) because it is a vital tool for digital goods and SaaS subscriptions selling globally. Scoring a 10/10 in Global Reach, it operates in over 200 countries. Crucially, its 2Monetize platform acts as a Merchant of Record, meaning 2Checkout assumes the massive legal burden of calculating and remitting global software taxes and VAT automatically.

Key Specs

- Available in 200+ countries and territories

- Optimized for SaaS and digital goods subscriptions

- Handles global tax and VAT compliance automatically

- Supports 45+ local payment methods

- Modular platform (2Sell, 2Subscribe, 2Monetize)

What we like

- Acts as a Merchant of Record to handle global VAT and tax entirely

- Incredible 200+ country availability

- Highly optimized for digital goods and SaaS subscriptions

What we don't like

- Standard transaction fees are very high (3.5% + 35¢)

- Not designed for physical retail or shipping physical goods

Best for: SaaS companies, software developers, and digital course creators selling globally.

Considering 2Checkout vs Stripe? Stripe is much cheaper for standard transactions, but 2Checkout handles global VAT and tax remittance completely as a Merchant of Record.

An essential global platform for digital goods sellers looking to completely offload international tax compliance.

Buy at 2Checkout official site#34 Merchant One

Why we picked it: We picked Merchant One because it boasts a remarkable 98% approval rate for new merchant accounts, making it a lifeline for businesses struggling with bad credit or slightly elevated risk profiles. Earning a 9/10 in Support, they assign a dedicated account manager to every merchant. While they operate on a tiered pricing model (which we usually penalize), their willingness to underwrite difficult accounts provides crucial market access.

Key Specs

- 98% approval rate for new merchant accounts

- Next-day funding capabilities

- Dedicated account managers assigned

- Free equipment provided with commitment

- Integrates with massive range of shopping carts

What we like

- Incredible 98% approval rate for difficult accounts

- Dedicated, personalized account management

- Offers free equipment with a signed agreement

What we don't like

- Relies on opaque tiered pricing structures

- Requires standard long-term contracts with cancellation fees

Best for: Merchants with thin credit files or unique business models who struggle to get approved elsewhere.

Considering Merchant One vs Helcim? Helcim is far more transparent and cheaper, but Merchant One is more likely to approve your account if you have poor credit.

A highly accommodating merchant account provider perfect for businesses struggling to secure processing approval.

Buy at Merchant One official site#35 QuickBooks Payments

Why we picked it: We picked QuickBooks Payments because it entirely eliminates the grueling manual data entry associated with bookkeeping. By integrating natively into QuickBooks Online, every swiped card or paid smart invoice automatically reconciles in your accounting ledger. While the flat 2.99% + 25¢ rate isn't the cheapest, the sheer amount of administrative hours saved makes it highly valuable for B2B service providers and contractors.

Key Specs

- Seamless integration with QuickBooks Online

- Pay-enabled smart invoices

- Auto-reconciliation saves bookkeeping hours

- ACH payments capped at low rates

- Next-day funding for eligible accounts

What we like

- Flawless, automatic reconciliation within QuickBooks

- Excellent pay-enabled smart invoicing

- Low capped fees for ACH bank transfers

What we don't like

- Processing rates are relatively high for flat-rate

- Customer service can be frustratingly generic

Best for: B2B service businesses, accountants, and contractors already running their operations on QuickBooks.

Considering QuickBooks Payments vs Square? Square is better for physical retail, while QuickBooks Payments is unparalleled for invoicing and automated accounting reconciliation.

The ultimate time-saving processor for B2B businesses that want their payments instantly reconciled in their accounting software.

Buy at QuickBooks official siteBuying Guide

Understanding Payment Processors vs. Merchant Accounts

Before selecting a platform, it is critical to understand the terminology. A Payment Gateway is the technology that captures and transfers payment data securely from the customer to the acquirer. A Payment Processor routes this data between the card networks and banks. Finally, a Merchant Account is a special business bank account that temporarily holds the funds before they are transferred to your primary business account. Modern Payment Service Providers (PSPs) like Stripe and PayPal bundle all three of these functions into a single, seamless platform, while traditional merchant acquirers require you to set them up separately but often provide lower, volume-based rates.

Pricing Models: What to Choose and What to Avoid

Payment processing fees are notorious for being complicated. Here are the three main pricing models to evaluate:

- Flat-Rate Pricing: Charges a fixed percentage plus a small cent fee per transaction (e.g., 2.9% + 30¢). This is highly predictable, requires no monthly commitment, and is excellent for low-volume or new businesses.

- Interchange-Plus Pricing: Passes the direct cost from the card network (the "interchange") directly to you, plus a transparent, fixed markup by the processor (e.g., Interchange + 0.15% + 10¢). This is generally the most cost-effective model for businesses processing over $10,000 per month.

- Tiered Pricing: Categorizes transactions into "qualified," "mid-qualified," and "non-qualified" tiers. Avoid this model. It is highly opaque, and processors often deliberately downgrade standard rewards cards to higher tiers to maximize their profits at your expense.

Choosing by Budget and Volume Tiers

If your business processes under $5,000 per month, an all-in-one PSP like Square, Stripe, or PayPal is typically the best fit because they do not charge monthly subscription fees and offer instant onboarding. However, if your business is scaling and processes upwards of $20,000 or $50,000 per month, subscription-based processors like Payment Depot or Stax (which charge a flat monthly fee in exchange for 0% markup on interchange rates) will save you thousands of dollars annually in processing markup fees.

Evaluating Checkout UX and Integrations

A clunky checkout interface directly causes cart abandonment. You need a payment processor that offers highly optimized mobile checkout flows, supports one-click digital wallets like Apple Pay and Google Pay natively, and integrates seamlessly with your existing tech stack (Shopify, WooCommerce, QuickBooks). Versatility matters: the best processors act as a unified commerce hub, effortlessly connecting online sales, brick-and-mortar operations, and backend accounting systems to eliminate manual data entry.

Security and Chargeback Mitigation

Security cannot be an afterthought. Look for processors that offer out-of-the-box PCI compliance, end-to-end tokenization, and robust machine learning tools (like Stripe Radar or Adyen RevenueProtect) to minimize fraudulent chargebacks without erroneously blocking legitimate customers.

FAQ

What is the difference between a payment gateway and a payment processor?

A payment gateway is the digital portal (like a card reader or website checkout) that securely encrypts and captures customer payment data. The payment processor is the actual financial engine that routes this encrypted data between the merchant's bank and the customer's card network (Visa, Mastercard) to authorize and settle the funds.

How do flat-rate vs. interchange-plus fees compare?

Flat-rate pricing charges a predictable, fixed amount (e.g., 2.9% + 30¢) regardless of the card type, making it great for low-volume startups. Interchange-plus pricing passes the actual card network cost to the merchant, plus a tiny, transparent processor markup. Interchange-plus is almost always cheaper for businesses processing over $10,000 per month.

What is the average funding speed for small business processors?

Most standard processors settle funds into a merchant's bank account within 2 business days. However, top-tier providers like Square, Chase Payment Solutions, and Stripe now offer next-business-day funding as standard, and instant payouts (within minutes) for an additional fee of around 1% to 1.5%.

How do I prevent fraudulent chargebacks?

To prevent chargebacks, utilize a payment processor that offers advanced Machine Learning fraud detection (like Stripe Radar or Adyen RevenueProtect). Ensure you are utilizing 3D Secure 2.0 authentication, collecting CVV codes, enforcing AVS (Address Verification System) matches, and explicitly stating your refund policies at checkout.

What are the best payment processors for high-volume businesses?

Businesses processing over $20,000 a month should avoid flat-rate processors like PayPal or standard Square. Instead, look to wholesale subscription processors like Payment Depot or Stax, which charge a flat monthly fee in exchange for 0% markup on raw interchange rates, generating massive savings.

Do I need a dedicated merchant account or a Payment Service Provider (PSP)?