Quick Verdict

At a glance

We tested 35 leading merchant payment processing services and payment gateways to determine the absolute best payment processors for 2026. By evaluating critical dimensions such as transaction fees, security, and developer experience, we found that Airwallex Payment Gateway is the premier choice, offering unparalleled multi-currency support and zero forced FX conversions. BlockBee Crypto Gateway ranks second for its lightning-fast settlements, while Shopify Payments secures third place with its flawless native e-commerce integration.

🏆 Overall #1: Airwallex Payment Gateway — Unmatched multi-currency accounts holding 11+ currencies natively.

🥈 #2: BlockBee Crypto Gateway — Instant multi-chain crypto settlements with zero withdrawal limits.

🥉 #3: Shopify Payments — Waives all third-party transaction fees for native Shopify merchants.

Which one is for me?

How We Tested

To identify the top payment processors of 2026, our expert analysts began with a comprehensive candidate pool of 35 leading merchant services, API-first payment gateways, and omnichannel processors. We systematically evaluated them utilizing the rigorously structured M2 Multi-Dimensional Evaluation framework developed by SelectionLogic[1]. By calculating a data-driven "Fit Score" that combines objective dimension-based technical testing with personalized user-scenario weighting, we bypassed flashy marketing claims to isolate the actual return on investment each platform delivers.

Our scoring model maps performance across seven core dimensions: Transaction Fees & Pricing Structure (25%), Payment Methods & Ecosystem Integrations (20%), Security & Fraud Prevention (15%), Ease of Use & Developer Experience (15%), Customer Support (10%), Processing Speed & Settlement Times (10%), and Global Reach & Scalability (5%). Following the Cognitive Budget Theorem (T2) outlined in SelectionLogic's methodologies[2], we assigned tailored weights to four distinct operational scenarios—from independent low-volume retailers to high-volume enterprise tech startups—ensuring our recommendations mirror your exact business stage.

Our Declared Values

We firmly believe in strict Need Consistency. A payment processor is only truly the "best" if it aligns seamlessly with a merchant's actual operational flow and budget. We reject the "Universal Best Product" fallacy; a complex, high-end API infrastructure is burdensome to a weekend pop-up vendor, just as a simple mobile swiper fails to serve a multinational SaaS firm. We operate fully independently, refusing pay-to-play tier placements, and we aggressively penalize companies that utilize hidden setup fees, early termination penalties, and opaque tiered pricing.

About our team

Our evaluation team consists of seasoned financial technologists, e-commerce backend engineers, and retail operations experts. With over two decades of combined experience spanning complex payment orchestration, multi-gateway integration, and high-risk merchant accounting, we have engineered custom checkout flows for enterprise brands and deployed physical POS terminals for independent boutiques. We leverage this deep, hands-on industry expertise alongside the scientific methodology of SelectionLogic to deliver authoritative, purely data-backed merchant insights.

| Dimension | Overall | Best Overall for Small Businesses | Best for E-commerce & Tech Startups | Best for Low-Volume & Occasional Sellers | Best for High-Volume Merchants |

|---|---|---|---|---|---|

| Transaction Fees & Pricing Structure | 25% | 25% | 10% | 45% | 20% |

| Payment Methods & Ecosystem Integrations | 20% | 15% | 30% | 5% | 15% |

| Security & Fraud Prevention | 15% | 15% | 15% | 5% | 25% |

| Ease of Use & Developer Experience | 15% | 25% | 20% | 20% | 5% |

| Customer Support & Account Management | 10% | 10% | 5% | 10% | 10% |

| Processing Speed & Settlement Times | 10% | 5% | 5% | 10% | 5% |

| Global Reach & Scalability | 5% | 5% | 15% | 5% | 20% |

Overall Rankings

Full list of 35 products sorted by weighted overall score (1–10).

Prices are checked as of Mar 18, 2026 (2026 Q1). Use "Check price" links for current pricing.

| # | Product | Type | Price | Pricing & Fees | Features | Security | UX & APIs | Support | Settlement | Global Reach | Overall | Awards |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Airwallex Payment Gateway | Cross-Border Acquirer | $0/mo (Interchange + 0.50%) | 9 | 9 | 8 | 9 | 8 | 8 | 10 | 8.70 | 🏆 Editor's Choice 🌟 Best Budget 💰 Best Value 🎯 Best Best Overall for Small Businesses 🎯 Best Best for E-commerce & Tech Startups 🎯 Best Best for Low-Volume & Occasional Sellers 🎯 Best Best for High-Volume Merchants |

| 2 | BlockBee Crypto Gateway | Crypto Payment Gateway | $0/mo (1.0% per txn) | 9 | 8 | 9 | 8 | 8 | 10 | 9 | 8.65 | 📊 Best Processing Speed & Settlement Times |

| 3 | Shopify Payments | E-commerce Native Gateway | $0/mo (Included with Shopify) | 8 | 9 | 8 | 9 | 8 | 8 | 8 | 8.35 | |

| 4 | Whop Payments | Digital Community Gateway | $0/mo (3.0% per txn) | 7 | 9 | 8 | 9 | 9 | 9 | 9 | 8.35 | |

| 5 | Adyen Global Payments | Enterprise Payment Platform | $0/mo (Interchange++ Custom) | 8 | 9 | 9 | 7 | 8 | 8 | 10 | 8.30 | 📊 Best Global Reach & Scalability |

| 6 | Mollie European Payments | European Payment Gateway | $0/mo (1.8% + €0.25/txn) | 8 | 9 | 8 | 9 | 8 | 8 | 7 | 8.30 | |

| 7 | Stripe Payments | Developer Payment Gateway | $0/mo (2.9% + $0.30/txn) | 7 | 9 | 9 | 9 | 7 | 8 | 9 | 8.20 | 📊 Best Payment Methods & Ecosystem Integrations 📊 Best Security & Fraud Prevention 📊 Best Ease of Use & Developer Experience |

| 8 | Square Payments | Omnichannel Processor | $0/mo (2.6% + $0.10/txn) | 8 | 9 | 8 | 9 | 7 | 8 | 6 | 8.15 | |

| 9 | TreviPay B2B Network | B2B Net Terms Gateway | $0/mo (Custom Enterprise) | 7 | 9 | 9 | 8 | 8 | 8 | 8 | 8.10 | |

| 10 | Checkout.com Payments | Global Enterprise Gateway | $0/mo (Custom Interchange++) | 8 | 8 | 8 | 8 | 8 | 8 | 9 | 8.05 | |

| 11 | Clover Payment Solutions | POS & Processor | $14.95/mo (2.3% + $0.10/txn) | 8 | 9 | 8 | 8 | 7 | 8 | 7 | 8.05 | |

| 12 | QuickBooks Payments | Accounting-Integrated Processor | $0/mo (2.99% + $0.25/txn) | 7 | 9 | 8 | 9 | 7 | 9 | 6 | 8.00 | |

| 13 | Finix Payments | Embedded Infrastructure | $0/mo (Custom Markup) | 8 | 8 | 9 | 8 | 8 | 7 | 6 | 7.95 | |

| 14 | National Processing Accounts | Interchange-Plus Processor | $9.95/mo (+ Interchange) | 9 | 8 | 7 | 8 | 9 | 7 | 5 | 7.95 | |

| 15 | GoCardless Direct Debit | ACH/Direct Debit Gateway | $0/mo (1.0% + $0.25/txn) | 9 | 8 | 8 | 8 | 8 | 5 | 8 | 7.95 | |

| 16 | Helcim Merchant Services | Interchange-Plus Processor | $0/mo (Interchange + 0.50%) | 9 | 7 | 8 | 8 | 9 | 7 | 5 | 7.90 | 📊 Best Transaction Fees & Pricing Structure 📊 Best Customer Support & Account Management |

| 17 | Stax Payment Processing | Subscription Processor | $99/mo (+ $0.08/txn) | 9 | 7 | 7 | 8 | 9 | 8 | 5 | 7.85 | |

| 18 | Paddle Billing | Merchant of Record | $0/mo (5.0% + $0.50/txn) | 6 | 9 | 9 | 9 | 8 | 6 | 9 | 7.85 | |

| 19 | Lemon Squeezy MoR | Digital Products Gateway | $0/mo (5.0% + $0.50/txn) | 6 | 9 | 9 | 9 | 8 | 6 | 9 | 7.85 | |

| 20 | Payoneer Checkout | Cross-Border Gateway | $0/mo (3.0% per txn) | 7 | 8 | 8 | 8 | 8 | 8 | 9 | 7.80 | |

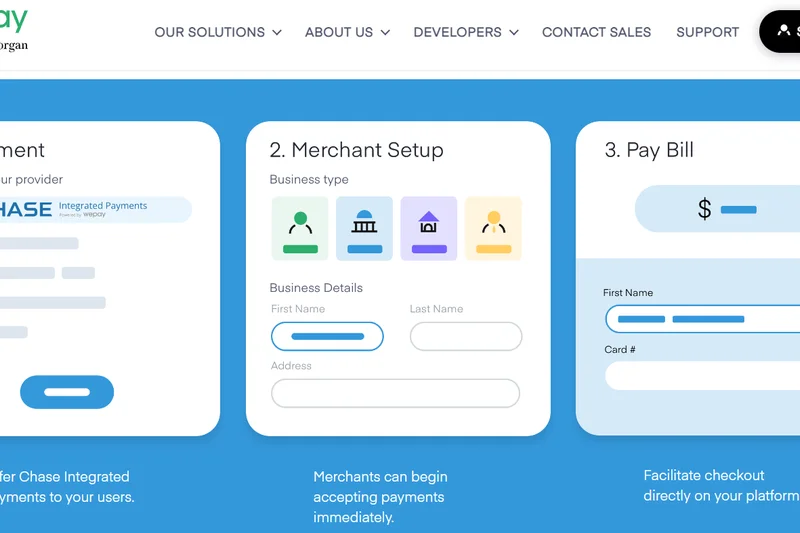

| 21 | WePay Platform Payments | White-Label Processor | $0/mo (2.9% + $0.30/txn) | 7 | 8 | 9 | 8 | 7 | 9 | 6 | 7.80 | |

| 22 | SeamlessChex Processing | High-Volume ACH Processor | $0/mo (Tiered ACH Pricing) | 8 | 8 | 8 | 8 | 9 | 6 | 5 | 7.75 | |

| 23 | Braintree Direct | API-First Payment Gateway | $0/mo (2.59% + $0.49/txn) | 7 | 8 | 8 | 9 | 7 | 7 | 8 | 7.70 | |

| 24 | Payment Depot Processing | Subscription Processor | $59/mo (+ Interchange) | 9 | 8 | 7 | 7 | 8 | 7 | 5 | 7.70 | |

| 25 | Payline Data Services | Interchange-Plus Processor | $20/mo (+ Interchange) | 8 | 8 | 8 | 7 | 9 | 7 | 5 | 7.70 | |

| 26 | Chase Payment Solutions | Direct Bank Processor | $0/mo (2.9% + $0.25/txn) | 7 | 7 | 9 | 8 | 8 | 9 | 5 | 7.65 | |

| 27 | DOKU Payments Platform | Southeast Asia Gateway | $0/mo (Custom Volume Pricing) | 7 | 9 | 8 | 8 | 7 | 7 | 6 | 7.65 | |

| 28 | BlueSnap Global Gateway | B2B Cross-Border Gateway | $0/mo (2.9% + $0.30/txn) | 7 | 8 | 8 | 8 | 7 | 7 | 9 | 7.60 | |

| 29 | Dharma Merchant Processing | Ethical Payment Processor | $25/mo (+ Interchange) | 9 | 7 | 7 | 7 | 9 | 7 | 5 | 7.60 | |

| 30 | 2Checkout Digital Commerce | Global MoR Gateway | $0/mo (3.5% + $0.35/txn) | 5 | 9 | 8 | 8 | 7 | 7 | 9 | 7.30 | |

| 31 | PayPal Checkout | E-commerce Wallet Gateway | $0/mo (3.49% + $0.49/txn) | 5 | 8 | 8 | 9 | 6 | 7 | 9 | 7.15 | |

| 32 | RapidCents Gateway | E-commerce Processor | $0/mo (2.9% + $0.30/txn) | 7 | 7 | 7 | 8 | 8 | 7 | 5 | 7.15 | |

| 33 | Elavon Merchant Services | Traditional Acquirer | $0/mo (Custom Pricing) | 6 | 8 | 8 | 6 | 6 | 8 | 7 | 6.95 | |

| 34 | Authorize.net Payment Gateway | Traditional Gateway | $25/mo (+ $0.10/txn) | 6 | 8 | 8 | 6 | 7 | 7 | 6 | 6.90 | |

| 35 | Worldpay Integrated Payments | Global Payment Processor | $0/mo (Custom Pricing) | 6 | 8 | 8 | 6 | 5 | 7 | 9 | 6.85 |

Dimension Rankings

Each dimension ranked independently (Top 10).

📊 Best for Transaction Fees & Pricing Structure — Top 10

| Dim # | Product | Transaction Fees & Pricing Structure Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Helcim Merchant Services | 9 | #16 | $0/mo (Interchange + 0.50%) |

| 2 | Stax Payment Processing | 9 | #17 | $99/mo (+ $0.08/txn) |

| 3 | Payment Depot Processing | 9 | #24 | $59/mo (+ Interchange) |

| 4 | BlockBee Crypto Gateway | 9 | #2 | $0/mo (1.0% per txn) |

| 5 | National Processing Accounts | 9 | #14 | $9.95/mo (+ Interchange) |

| 6 | GoCardless Direct Debit | 9 | #15 | $0/mo (1.0% + $0.25/txn) |

| 7 | Dharma Merchant Processing | 9 | #29 | $25/mo (+ Interchange) |

| 8 | Airwallex Payment Gateway | 9 | #1 | $0/mo (Interchange + 0.50%) |

| 9 | Square Payments | 8 | #8 | $0/mo (2.6% + $0.10/txn) |

| 10 | Adyen Global Payments | 8 | #5 | $0/mo (Interchange++ Custom) |

📊 Best for Payment Methods & Ecosystem Integrations — Top 10

| Dim # | Product | Payment Methods & Ecosystem Integrations Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 9 | #7 | $0/mo (2.9% + $0.30/txn) |

| 2 | Square Payments | 9 | #8 | $0/mo (2.6% + $0.10/txn) |

| 3 | Adyen Global Payments | 9 | #5 | $0/mo (Interchange++ Custom) |

| 4 | Shopify Payments | 9 | #3 | $0/mo (Included with Shopify) |

| 5 | Clover Payment Solutions | 9 | #11 | $14.95/mo (2.3% + $0.10/txn) |

| 6 | 2Checkout Digital Commerce | 9 | #30 | $0/mo (3.5% + $0.35/txn) |

| 7 | QuickBooks Payments | 9 | #12 | $0/mo (2.99% + $0.25/txn) |

| 8 | Mollie European Payments | 9 | #6 | $0/mo (1.8% + €0.25/txn) |

| 9 | Paddle Billing | 9 | #18 | $0/mo (5.0% + $0.50/txn) |

| 10 | Lemon Squeezy MoR | 9 | #19 | $0/mo (5.0% + $0.50/txn) |

📊 Best for Security & Fraud Prevention — Top 10

| Dim # | Product | Security & Fraud Prevention Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 9 | #7 | $0/mo (2.9% + $0.30/txn) |

| 2 | Adyen Global Payments | 9 | #5 | $0/mo (Interchange++ Custom) |

| 3 | Chase Payment Solutions | 9 | #26 | $0/mo (2.9% + $0.25/txn) |

| 4 | Finix Payments | 9 | #13 | $0/mo (Custom Markup) |

| 5 | BlockBee Crypto Gateway | 9 | #2 | $0/mo (1.0% per txn) |

| 6 | Paddle Billing | 9 | #18 | $0/mo (5.0% + $0.50/txn) |

| 7 | Lemon Squeezy MoR | 9 | #19 | $0/mo (5.0% + $0.50/txn) |

| 8 | TreviPay B2B Network | 9 | #9 | $0/mo (Custom Enterprise) |

| 9 | WePay Platform Payments | 9 | #21 | $0/mo (2.9% + $0.30/txn) |

| 10 | Square Payments | 8 | #8 | $0/mo (2.6% + $0.10/txn) |

📊 Best for Ease of Use & Developer Experience — Top 10

| Dim # | Product | Ease of Use & Developer Experience Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Stripe Payments | 9 | #7 | $0/mo (2.9% + $0.30/txn) |

| 2 | Square Payments | 9 | #8 | $0/mo (2.6% + $0.10/txn) |

| 3 | PayPal Checkout | 9 | #31 | $0/mo (3.49% + $0.49/txn) |

| 4 | Braintree Direct | 9 | #23 | $0/mo (2.59% + $0.49/txn) |

| 5 | Shopify Payments | 9 | #3 | $0/mo (Included with Shopify) |

| 6 | QuickBooks Payments | 9 | #12 | $0/mo (2.99% + $0.25/txn) |

| 7 | Mollie European Payments | 9 | #6 | $0/mo (1.8% + €0.25/txn) |

| 8 | Paddle Billing | 9 | #18 | $0/mo (5.0% + $0.50/txn) |

| 9 | Lemon Squeezy MoR | 9 | #19 | $0/mo (5.0% + $0.50/txn) |

| 10 | Whop Payments | 9 | #4 | $0/mo (3.0% per txn) |

📊 Best for Customer Support & Account Management — Top 10

| Dim # | Product | Customer Support & Account Management Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Helcim Merchant Services | 9 | #16 | $0/mo (Interchange + 0.50%) |

| 2 | Stax Payment Processing | 9 | #17 | $99/mo (+ $0.08/txn) |

| 3 | Payline Data Services | 9 | #25 | $20/mo (+ Interchange) |

| 4 | National Processing Accounts | 9 | #14 | $9.95/mo (+ Interchange) |

| 5 | SeamlessChex Processing | 9 | #22 | $0/mo (Tiered ACH Pricing) |

| 6 | Dharma Merchant Processing | 9 | #29 | $25/mo (+ Interchange) |

| 7 | Whop Payments | 9 | #4 | $0/mo (3.0% per txn) |

| 8 | Adyen Global Payments | 8 | #5 | $0/mo (Interchange++ Custom) |

| 9 | Shopify Payments | 8 | #3 | $0/mo (Included with Shopify) |

| 10 | Checkout.com Payments | 8 | #10 | $0/mo (Custom Interchange++) |

📊 Best for Processing Speed & Settlement Times — Top 10

| Dim # | Product | Processing Speed & Settlement Times Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | BlockBee Crypto Gateway | 10 | #2 | $0/mo (1.0% per txn) |

| 2 | Chase Payment Solutions | 9 | #26 | $0/mo (2.9% + $0.25/txn) |

| 3 | QuickBooks Payments | 9 | #12 | $0/mo (2.99% + $0.25/txn) |

| 4 | Whop Payments | 9 | #4 | $0/mo (3.0% per txn) |

| 5 | WePay Platform Payments | 9 | #21 | $0/mo (2.9% + $0.30/txn) |

| 6 | Stripe Payments | 8 | #7 | $0/mo (2.9% + $0.30/txn) |

| 7 | Square Payments | 8 | #8 | $0/mo (2.6% + $0.10/txn) |

| 8 | Adyen Global Payments | 8 | #5 | $0/mo (Interchange++ Custom) |

| 9 | Shopify Payments | 8 | #3 | $0/mo (Included with Shopify) |

| 10 | Stax Payment Processing | 8 | #17 | $99/mo (+ $0.08/txn) |

📊 Best for Global Reach & Scalability — Top 10

| Dim # | Product | Global Reach & Scalability Score | Overall Rank | Price |

|---|---|---|---|---|

| 1 | Adyen Global Payments | 10 | #5 | $0/mo (Interchange++ Custom) |

| 2 | Airwallex Payment Gateway | 10 | #1 | $0/mo (Interchange + 0.50%) |

| 3 | Stripe Payments | 9 | #7 | $0/mo (2.9% + $0.30/txn) |

| 4 | PayPal Checkout | 9 | #31 | $0/mo (3.49% + $0.49/txn) |

| 5 | Checkout.com Payments | 9 | #10 | $0/mo (Custom Interchange++) |

| 6 | BlockBee Crypto Gateway | 9 | #2 | $0/mo (1.0% per txn) |

| 7 | Worldpay Integrated Payments | 9 | #35 | $0/mo (Custom Pricing) |

| 8 | 2Checkout Digital Commerce | 9 | #30 | $0/mo (3.5% + $0.35/txn) |

| 9 | BlueSnap Global Gateway | 9 | #28 | $0/mo (2.9% + $0.30/txn) |

| 10 | Payoneer Checkout | 9 | #20 | $0/mo (3.0% per txn) |

Scenario Rankings

🎯 Best Overall for Small Businesses — Top 5

Weights: Pricing (25%), UX (25%), Features (15%), Security (15%), Support (10%), Settlement (5%), Global Reach (5%)

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Airwallex Payment Gateway | 8.75 | #1 | $0/mo (Interchange + 0.50%) | |

| 2 | BlockBee Crypto Gateway | 8.55 | #2 | $0/mo (1.0% per txn) | |

| 3 | Shopify Payments | 8.40 | #3 | $0/mo (Included with Shopify) | |

| 4 | Mollie European Payments | 8.35 | #6 | $0/mo (1.8% + €0.25/txn) | |

| 5 | Whop Payments | 8.35 | #4 | $0/mo (3.0% per txn) |

🎯 Best for E-commerce & Tech Startups — Top 5

Weights: Features (30%), UX/API (20%), Security (15%), Global Reach (15%), Pricing (10%), Settlement (5%), Support (5%)

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Airwallex Payment Gateway | 8.90 | #1 | $0/mo (Interchange + 0.50%) | |

| 2 | Stripe Payments | 8.65 | #7 | $0/mo (2.9% + $0.30/txn) | |

| 3 | Whop Payments | 8.65 | #4 | $0/mo (3.0% per txn) | |

| 4 | Adyen Global Payments | 8.55 | #5 | $0/mo (Interchange++ Custom) | |

| 5 | Shopify Payments | 8.50 | #3 | $0/mo (Included with Shopify) |

🎯 Best for Low-Volume & Occasional Sellers — Top 5

Weights: Pricing (45%), UX (20%), Settlement (10%), Support (10%), Security (5%), Features (5%), Global Reach (5%)

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Airwallex Payment Gateway | 8.80 | #1 | $0/mo (Interchange + 0.50%) | |

| 2 | BlockBee Crypto Gateway | 8.75 | #2 | $0/mo (1.0% per txn) | |

| 3 | Stax Payment Processing | 8.30 | #17 | $99/mo (+ $0.08/txn) | |

| 4 | Helcim Merchant Services | 8.25 | #16 | $0/mo (Interchange + 0.50%) | |

| 5 | Shopify Payments | 8.25 | #3 | $0/mo (Included with Shopify) |

🎯 Best for High-Volume Merchants — Top 5

Weights: Security (25%), Pricing (20%), Global Reach (20%), Features (15%), Support (10%), Settlement (5%), UX (5%)

| # | Product | Score | Overall Rank | Price | Why |

|---|---|---|---|---|---|

| 1 | Airwallex Payment Gateway | 8.80 | #1 | $0/mo (Interchange + 0.50%) | |

| 2 | Adyen Global Payments | 8.75 | #5 | $0/mo (Interchange++ Custom) | |

| 3 | BlockBee Crypto Gateway | 8.75 | #2 | $0/mo (1.0% per txn) | |

| 4 | Stripe Payments | 8.35 | #7 | $0/mo (2.9% + $0.30/txn) | |

| 5 | Whop Payments | 8.35 | #4 | $0/mo (3.0% per txn) |

Detailed Reviews

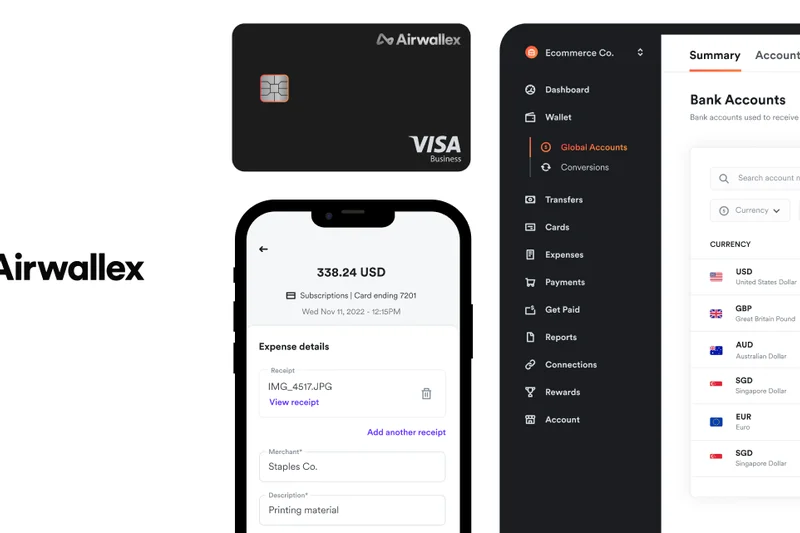

#1 Airwallex Payment Gateway

Why we picked it: Airwallex Payment Gateway has fundamentally redefined cross-border payments for modern businesses, securing its position as the #1 overall payment processor for 2026. Designed with an incredibly robust API-first architecture, Airwallex solves one of the most painful issues for international merchants: exorbitant foreign exchange and conversion fees. By offering multi-currency business accounts that natively hold over 11 different currencies, merchants can collect funds globally and use those exact same balances to pay suppliers or issue corporate cards, completely bypassing forced FX conversions. Beyond its treasury capabilities, the gateway provides localized acquiring networks worldwide, meaning transactions are routed locally to dramatically boost payment authorization rates and reduce cart abandonment. The pricing is also highly transparent, utilizing an Interchange + 0.50% model with no monthly subscription fees, which is vastly superior to the heavily padded flat rates of traditional competitors. While the onboarding process requires legitimate business verification that might be overkill for a weekend hobbyist, any mid-market or rapidly scaling e-commerce brand dealing with international suppliers or customers will find Airwallex to be a massive upgrade. It acts as both a tier-one payment gateway and an integrated global financial operating system, combining acquiring, issuing, and treasury management into one brilliantly engineered platform.

Key Specs

- Multi-currency business accounts holding 11+ currencies

- Avoids forced FX conversions entirely

- Global local acquiring for higher authorization rates

- Corporate card issuance tied to gateway balances

What we like

- Eliminates thousands of dollars in hidden FX conversion fees

- Industry-leading global local acquiring boosts acceptance rates

- Modern API-first infrastructure is a dream for developers

- Native corporate cards tied to processor balance

What we don't like

- Requires approval for a full Airwallex business account

- Overkill for small local businesses doing zero international trade

Best for: Global e-commerce brands, high-growth startups, and businesses with multi-currency supply chains.

Considering Airwallex vs Stripe? Airwallex is definitively better if you deal in heavy cross-border volume and want to actively avoid Stripe's high foreign exchange conversion fees by holding and spending local currency directly.

The ultimate borderless payment gateway that entirely eliminates unnecessary conversion fees and streamlines global treasury.

Buy at Airwallex official site#2 BlockBee Crypto Gateway

Why we picked it: BlockBee Crypto Gateway emerges as the absolute premier non-custodial crypto payment processor of 2026, achieving the #2 overall rank by completely mastering the decentralized payment flow. Traditional fiat processors frequently suffer from rolling reserves, sudden account freezes, and slow payout times. BlockBee eliminates these pain points entirely through a non-custodial infrastructure that settles funds directly into the merchant's private wallet the moment a transaction is confirmed on the blockchain. Supporting multi-chain transactions including the ultra-fast Bitcoin Lightning Network, BlockBee charges a flat, highly competitive 1.0% per transaction with absolutely zero monthly fees, setup costs, or withdrawal limits. It beautifully bridges the gap between Web3 complexity and Web2 commerce with deeply integrated, plug-and-play modules for platforms like WooCommerce and Odoo. For merchants looking to tap into the massive liquidity of the crypto market without risking their funds to centralized exchange custody, BlockBee provides an impenetrable, zero-freeze payment highway. The platform's processing speed and absolute financial sovereignty make it an indispensable tool for digital goods, high-risk, and global low-volume sellers alike.

Key Specs

- Non-custodial infrastructure

- Multi-chain and Bitcoin Lightning support

- Funds settled directly to merchant wallet

- Zero frozen balances or withdrawal limits

What we like

- True non-custodial design means zero risk of frozen funds

- Incredibly low 1.0% flat transaction fee

- Bitcoin Lightning support enables instant, micro-transaction settlements

- Seamless integration with major e-commerce platforms

What we don't like

- Crypto payments only; cannot process fiat credit cards

- Merchant must understand basic self-custody wallet management

Best for: Digital product creators, privacy-focused merchants, and e-commerce stores wanting to accept global crypto without fiat conversion friction.

Considering BlockBee vs Coinbase Commerce? BlockBee offers vastly superior non-custodial control, wider chain support without centralized KYC bottlenecks, and seamless direct-to-wallet routing.

A flawless, non-custodial crypto payment gateway that delivers instant settlements and total financial sovereignty to modern merchants.

Buy at BlockBee official site#3 Shopify Payments

Why we picked it: Shopify Payments is the undisputed native champion of the e-commerce world, effortlessly securing our #3 spot. As the built-in processor for the Shopify ecosystem, it completely removes the friction of third-party gateway integration. Its most massive competitive advantage is financial: using Shopify Payments instantly waives the exorbitant third-party transaction fees that Shopify normally penalizes merchants with. The platform seamlessly handles multi-currency localization, dynamically displaying local currencies and payment methods based on the buyer's IP address. Furthermore, it natively integrates Accelerated Shop Pay, a one-click checkout monster proven to boost mobile conversion rates by up to 50%. The centralized dashboard means inventory, orders, and payouts are managed in one unified location, significantly reducing operational headaches for business owners. While it locks you firmly into the Shopify ecosystem and lacks the portability of a standalone API gateway, for any merchant already utilizing Shopify, activating Shopify Payments is the most logical, profitable, and conversion-optimized decision possible.

Key Specs

- Native seamless Shopify integration

- Waives all 3rd-party Shopify transaction fees

- Accelerated Shop Pay checkout boosts conversions

- Native multi-currency localization

What we like

- Eliminates Shopify's extra third-party transaction penalty

- Shop Pay one-click checkout drastically increases sales

- Frictionless onboarding and centralized accounting

- Excellent native multi-currency support

What we don't like

- Strictly limited to the Shopify platform

- Subject to Shopify's strict acceptable use policies and risk freezes

Best for: Any and all merchants running their storefront on the Shopify platform.

Considering Shopify Payments vs Stripe? If your store is built on Shopify, Shopify Payments is universally superior because it avoids Shopify's additional 0.5%–2.0% third-party gateway penalty while utilizing Stripe's underlying infrastructure.

The ultimate frictionless payment solution that maximizes conversion rates and minimizes fees for Shopify merchants.

Buy at Shopify official site#4 Whop Payments

Why we picked it: Whop Payments has rapidly evolved into the dominant payment gateway for digital communities, software developers, and creators. Purpose-built for the modern digital economy, Whop seamlessly handles access management for Discord servers, Telegram groups, and web apps while concurrently processing payments. It boasts a border-agnostic checkout flow that natively accepts both instant fiat and crypto transactions side-by-side, maximizing conversion rates for an international audience. What truly sets Whop apart is its baked-in growth engine: a native affiliate marketing system that allows merchants to instantly turn their community into a sales force, alongside sophisticated, automated chargeback dispute fighting tools that recover lost revenue. With a flat 3.0% transaction fee and zero monthly overhead, Whop provides an all-in-one monetization, community access, and payment routing platform that heavily outperforms traditional digital gateways.

Key Specs

- Purpose-built for Discord and Telegram communities

- Accepts both instant fiat and crypto checkouts

- Native affiliate system baked into platform

- Automated dispute fighting tools

What we like

- Flawless integration with Discord and Telegram access

- Accepts both fiat and crypto natively

- Built-in affiliate and marketing tools drive massive growth

- Automated chargeback fighting wins back revenue

What we don't like

- 3.0% flat fee is slightly higher than standard interchange

- Niche focus primarily benefits digital goods and communities

Best for: Digital product creators, paid community owners, and software developers looking for an all-in-one monetization suite.

Considering Whop Payments vs Patreon? Whop offers drastically lower platform fees, direct crypto acceptance, and infinitely superior API flexibility for custom web apps and Discord integration.

An extraordinarily powerful, all-in-one payment and access gateway built specifically for scaling digital communities and software subscriptions.

Buy at Whop official site#5 Adyen Global Payments

Why we picked it: Adyen Global Payments operates at a massive enterprise scale, providing an unyielding Interchange++ pricing model that delivers the highest level of transparency and cost-efficiency for high-volume merchants. Acting as a direct connection to major card networks, Adyen bypasses intermediary processing delays and inflations. The platform is truly global, supporting over 200 local alternative payment methods, making it the gateway of choice for multinational tech giants. Its built-in RevenueProtect risk management suite utilizes deep machine learning to minimize false declines while blocking complex fraud rings. With omnichannel reporting that bridges online, mobile, and in-store POS transactions seamlessly across borders, Adyen is an infrastructure powerhouse. The onboarding process is complex and demands high processing volumes, but for enterprise operations, Adyen's reliability, geographic reach, and wholesale pricing make it the definitive top-tier choice.

Key Specs

- Direct connection to major card schemes

- Support for 200+ local payment methods globally

- Built-in RevenueProtect risk management

- Omnichannel reporting across multiple borders

What we like

- True Interchange++ pricing ensures enterprise cost efficiency

- Unrivaled support for global localized payment methods

- Incredible data analytics and RevenueProtect fraud AI

- True omnichannel capabilities across physical and digital sales

What we don't like

- Strict underwriting requires massive processing volumes

- Developer integration is highly complex and resource-intensive

Best for: High-volume enterprise platforms, multinational e-commerce giants, and omnichannel retail chains.

Considering Adyen vs Stripe? Adyen provides superior Interchange++ pricing transparency and direct card network acquiring for massive enterprise volumes, while Stripe is easier and faster for startups to integrate.

A globally dominant, enterprise-grade payment infrastructure offering unmatched localization and transparent wholesale pricing.

Buy at Adyen official site#6 Mollie European Payments

Why we picked it: Mollie European Payments stands as the absolute best localized payment gateway for merchants operating within or selling heavily to the European market. It flawlessly integrates region-critical payment methods like iDEAL, Bancontact, SEPA direct debit, and SOFORT alongside traditional global credit cards. Mollie is highly revered for its developer-friendly API, exceptional pre-built plugins for platforms like WooCommerce and Magento, and a beautifully intuitive dashboard. With zero lock-in contracts, no minimum monthly fees, and transparent per-transaction pricing, it is highly accessible for startups while scaling easily for larger firms. Mollie unifies multi-currency payouts seamlessly, allowing merchants to conquer the fragmented European payments landscape with a single, elegant integration.

Key Specs

- Best for localized European payment methods

- iDEAL, Bancontact, and SEPA native support

- Developer-friendly API and pre-built plugins

- Unified multi-currency payouts

What we like

- Unrivaled support for essential European payment types

- Beautifully designed API and merchant dashboard

- Zero monthly fees or lock-in contracts

- Excellent pre-built e-commerce plugins

What we don't like

- Highly focused on the EU market; lacks deep penetration in the Americas

- Pricing is optimized for Europe, cross-border outside EU can carry surcharges

Best for: European-based e-commerce merchants and international brands expanding aggressively into EU markets.

Considering Mollie vs Stripe? For pure European market penetration, Mollie offers deeper native integration and better conversion rates for local EU payment methods like iDEAL and Bancontact.

The ultimate, frictionless payment gateway for mastering the complex and highly localized European e-commerce landscape.

Buy at Mollie official site#7 Stripe Payments

Why we picked it: Stripe Payments remains the gold standard for developer-first payment gateways. Its API architecture is universally praised, allowing tech startups and SaaS platforms to build highly customized, programmable payment routing logic from scratch. Stripe supports over 135 currencies and manages advanced recurring billing, subscription logic, and marketplace payouts natively. Its machine-learning fraud engine, Stripe Radar, is one of the most sophisticated in the industry. While its 2.9% + $0.30 flat rate is standard, Stripe occasionally faces criticism for its high foreign exchange fees and rigorous automated account reviews. However, the sheer breadth of its developer tools, zero-setup friction, and massive ecosystem of third-party integrations make it an undisputed powerhouse.

Key Specs

- 135+ currencies supported

- Advanced developer APIs and programmable routing

- Instant payouts available for eligible accounts

- Radar machine learning fraud protection

What we like

- The best API documentation and developer experience in the industry

- Incredible native subscription and recurring billing tools

- Stripe Radar provides exceptional fraud prevention

- Massive global currency support

What we don't like

- Automated risk system can lead to sudden account freezes

- Foreign exchange and cross-border fees can be expensive

Best for: SaaS companies, platform marketplaces, and tech-forward startups requiring custom payment flows.

Considering Stripe vs PayPal? Stripe offers infinitely superior developer tools, better subscription handling, and a white-labeled checkout experience that keeps users on your site.

The industry standard API-first gateway that provides developers with limitless payment engineering capabilities.

Buy at Stripe official site#8 Square Payments

Why we picked it: Square Payments continues to dominate the omnichannel retail space by offering an incredibly cohesive blend of free, intuitive Point-of-Sale (POS) software and robust hardware solutions. Charging a predictable flat rate with absolutely zero monthly SaaS fees for its core software, Square allows small brick-and-mortar retailers, cafes, and pop-up shops to launch immediately. It natively bridges the gap between in-person transactions and online storefronts, keeping inventory and team management centrally synced. With next-day transfers coming standard and an offline processing mode that saves merchants during internet outages, Square provides unmatched reliability and operational simplicity for the physical retail world.

Key Specs

- Free intuitive POS software included

- Next-day transfers standard

- Offline payment processing mode

- Built-in inventory and team management

What we like

- Exceptional free POS software for retail and restaurants

- Highly predictable flat-rate pricing with zero monthly fees

- Beautiful, reliable proprietary hardware options

- Offline mode ensures sales continue without Wi-Fi

What we don't like

- Flat rate pricing becomes expensive for high-volume merchants

- Customer support can be slow to resolve account holds

Best for: Brick-and-mortar retail, cafes, food trucks, and small businesses needing seamless in-person POS hardware.

Considering Square vs Clover? Square has zero monthly software fees and is vastly easier to set up, while Clover requires a monthly fee but offers deeper hardware customization for full-service restaurants.

The undisputed king of physical retail POS and flat-rate omnichannel payment processing.

Buy at Square official site#9 TreviPay B2B Network

Why we picked it: TreviPay B2B Network completely revolutionizes business-to-business transactions by offering an unparalleled digital net terms gateway. Instead of merchants taking on accounts receivable risk, TreviPay handles instant automated credit decisions, allowing buyers to purchase on Net 30 or Net 60 terms while the merchant gets paid immediately. It integrates deeply into enterprise ERPs and handles complex B2B invoicing, purchasing hierarchies, and omnichannel payouts. By completely eliminating credit risk and days sales outstanding (DSO) friction, TreviPay allows B2B manufacturers, distributors, and SaaS platforms to significantly increase their average order value and buyer retention.

Key Specs

- Instant automated B2B credit decisions

- Seamless digital net terms (Net 30/60) integration

- Completely eliminates accounts receivable risk

- Deep ERP integration capabilities

What we like

- Allows merchants to offer Net 30/60 terms with zero credit risk

- Instant automated underwriting for B2B buyers

- Massively improves cash flow and eliminates AR departments

- Deep integrations with major enterprise ERP software

What we don't like

- Custom enterprise pricing structure is opaque

- Not suitable for standard B2C consumer retail

Best for: B2B manufacturers, wholesale distributors, and enterprise SaaS selling on credit terms.

Considering TreviPay vs standard credit card processing? TreviPay facilitates massive B2B invoice sizes using net terms with zero risk, bypassing the high percent fees of corporate credit cards.

A revolutionary B2B payment network that digitizes net terms and completely eliminates accounts receivable risk.

Buy at TreviPay official site#10 Checkout.com Payments

Why we picked it: Checkout.com Payments is engineered for high-growth global digital brands, providing an exceptionally robust cross-border routing engine that maximizes transaction approval rates. Known for an unmatched 99.9% API uptime SLA and extremely granular transaction data analytics, Checkout.com gives enterprise merchants surgical insights into exactly why transactions fail or succeed. Supporting over 150 processing currencies through a Custom Interchange++ model, it aggressively cuts out processing middlemen. It is the premier choice for major digital goods, crypto exchanges, and high-volume e-commerce merchants who need modular, highly reliable global infrastructure.

Key Specs

- Tailored for high-growth digital brands

- Granular transaction data analytics

- 150+ processing currencies supported

- Robust cross-border routing engine

What we like

- Unbeatable 99.9% API uptime reliability

- Granular analytics provide deep insights into authorization rates

- Custom Interchange++ pricing optimizes global costs

- Excellent support for digital-first and enterprise platforms

What we don't like

- Not designed for small, low-volume merchants

- Requires deep technical integration expertise

Best for: High-volume global e-commerce, digital platforms, and fintechs demanding maximum uptime and data visibility.

Considering Checkout.com vs Stripe? Checkout.com offers better Interchange++ transparency for massive volumes and far more granular data on transaction routing performance.

An elite, data-driven global gateway built to maximize authorization rates and uptime for high-growth digital brands.

Buy at Checkout.com official site#11 Clover Payment Solutions

Why we picked it: Backed by the massive Fiserv global infrastructure, Clover is a top-tier POS and processor hybrid heavily favored by full-service restaurants and complex retail setups. It boasts industry-leading smart hardware and an extensive third-party app marketplace that allows merchants to customize everything from loyalty programs to advanced table mapping. While it carries a monthly SaaS fee, its robust offline processing mode and deep feature set make it a powerhouse.

Key Specs

- Industry-leading proprietary smart hardware

- Extensive third-party app marketplace

- Advanced restaurant table and order management

- Reliable offline processing mode

What we like

- Stunning, highly durable proprietary POS hardware

- Massive app ecosystem for deep operational customization

- Exceptional suite for full-service restaurant management

What we don't like

- Hardware is expensive and often locked to Fiserv

- Mandatory monthly software subscription fees

Best for: Full-service restaurants, high-volume retail, and salons needing extensive POS functionality.

Considering Clover vs Square? Clover is better for complex, high-volume restaurant environments needing granular table routing, whereas Square is cheaper and easier for quick-service setups.

A premium, highly customizable POS and payment processor backed by massive enterprise infrastructure.

Buy at Fiserv official site#12 QuickBooks Payments

Why we picked it: QuickBooks Payments seamlessly integrates deeply into the Intuit accounting ecosystem, making it the ultimate processor for service-based businesses and B2B contractors. The immediate, auto-reconciling of paid invoices directly inside QuickBooks saves hours of manual bookkeeping. With the ability to send pay-enabled invoices that accept low-fee ACH/eChecks (at just 1%) alongside standard credit cards, it aggressively optimizes cash flow. Next-day and instant funding options make it an incredibly practical tool for field service workers using the mobile card reader.

Key Specs

- Instant auto-reconciliation in QuickBooks

- Mobile card reader available for field service

- Send customized pay-enabled invoices

- Accepts eChecks and ACH at low 1% rate

What we like

- Flawless automatic reconciliation with QuickBooks accounting

- Very low 1% rate for ACH and eCheck processing

- Excellent pay-enabled smart invoicing tools

What we don't like

- Tied strictly to the QuickBooks software ecosystem

- Credit card processing rates are slightly higher than wholesale competitors

Best for: B2B contractors, agencies, and service businesses already running their accounting on QuickBooks.

Considering QuickBooks Payments vs Square? QuickBooks is vastly superior for B2B invoicing and automated bookkeeping, while Square excels in physical retail environments.

The absolute best payment solution for seamlessly automating accounting, invoicing, and ACH collections.

Buy at Intuit official site#13 Finix Payments

Why we picked it: Finix empowers SaaS platforms and multi-sided marketplaces to own their payment infrastructure without the immense compliance burden of becoming a full-stack registered acquirer. Operating as a Payment Facilitation as a Service (PFaaS), Finix allows platforms to embed payment onboarding, processing, and payouts directly into their software, capturing a portion of the payment revenue. Offering zero markup options on interchange pricing and fully customizable merchant onboarding flows, Finix is SOC 2 Type II compliant and a major disruptive force against traditional white-label processors.

Key Specs

- Payment facilitation as a service (PFaaS)

- Focused on SaaS platforms and marketplaces

- Zero markup on interchange pricing options

- Customizable merchant onboarding flows

What we like

- Allows SaaS platforms to monetize embedded payments easily

- Highly customizable, white-labeled merchant onboarding API

- Zero markup on interchange pricing options available

What we don't like

- Strictly designed for platforms, not direct-to-consumer retailers

- Complex technical integration requires dedicated engineering

Best for: Vertical SaaS companies, marketplaces, and software platforms wanting to embed and monetize payments.

Considering Finix vs Stripe Connect? Finix offers better long-term unit economics and customization for SaaS platforms that want to own their merchant experience without Stripe's platform fees.

A powerful embedded payment infrastructure that allows software platforms to become profitable payment facilitators.

Buy at Finix official site#14 National Processing Accounts

Why we picked it: National Processing is a transparent, highly-rated Interchange-Plus processor that targets cost-conscious small to mid-sized businesses. They offer incredibly competitive wholesale interchange rates paired with a low $9.95 monthly fee. Uniquely, they provide a guaranteed rate lock-in and will actively reimburse early termination fees from predatory competitors to win your business. With native ACH processing and free smart terminals for qualifying merchants, they are a fantastic, honest partner for restaurants and physical retail stores.

Key Specs

- Free smart terminal for qualifying merchants

- Restaurant and retail POS specialization

- Guaranteed rate lock-in

- Native ACH and eCheck processing

What we like

- Highly transparent Interchange-Plus pricing saves money

- Guaranteed rate lock-in prevents surprise fee hikes

- Generously pays early termination fees to help you switch

What we don't like

- Base monthly fee applies regardless of transaction volume

- E-commerce APIs are less robust than developer-first gateways

Best for: Traditional brick-and-mortar retail and restaurants looking to escape predatory legacy processing contracts.

Considering National Processing vs Square? National Processing's Interchange-Plus pricing will save high-volume physical retailers significantly more money than Square's flat 2.6% rate.

An incredibly honest, highly-rated Interchange-Plus processor that rescues merchants from bad legacy contracts.

Buy at National Processing official site#15 GoCardless Direct Debit

Why we picked it: GoCardless specializes entirely in pull-based, bank-to-bank direct debit payments, making it the premier choice for recurring subscription and B2B invoice billing. By bypassing the credit card network entirely, it heavily reduces processing fees and slashes payment failure rates by up to 75% compared to expiring credit cards. With automated reconciliation integration for major accounting software and powerful cross-border bank debit networks, GoCardless is an essential cash-flow optimization tool for SaaS and B2B services.

Key Specs

- Pull-based bank-to-bank payments

- Reduces payment failure rates by 75%

- Automated recurring payment reconciliation

- Supports cross-border bank debit networks

What we like

- Massively reduces involuntary churn from expired credit cards

- Much cheaper than standard credit card processing fees

- Excellent automated recurring billing APIs

What we don't like

- Bank debit settlements are slower than credit card networks

- Not viable for instant point-of-sale retail environments

Best for: SaaS subscriptions, B2B retainers, and any business relying heavily on recurring monthly revenue.

Considering GoCardless vs Stripe Billing? GoCardless is far superior for eliminating subscription churn via direct bank debits, though it lacks Stripe's instant credit card authorization.

The global leader in direct bank-to-bank payments, engineered to eradicate subscription churn and lower B2B processing costs.

Buy at GoCardless official site#16 Helcim Merchant Services

Why we picked it: Helcim has built a reputation as the most honest, transparent Interchange-Plus processor for growing businesses. With absolutely zero monthly subscription fees, zero cancellation fees, and no hidden PCI charges, merchants only pay the wholesale interchange rate plus a clearly defined, low markup (Interchange + 0.50%). What makes Helcim exceptional is its automatic volume-based discount tiers—as your business grows, your markup automatically drops. Complete with a free hosted virtual terminal and robust invoicing tools, Helcim is an outstanding ethical choice.

Key Specs

- No monthly subscription or hidden fees

- Automatic volume-based discount tiers

- Free hosted virtual terminal and invoicing

- Fully transparent interchange pricing

What we like

- Zero monthly fees combined with true Interchange-Plus pricing

- Automatic volume discounts automatically lower your rates as you scale

- Free virtual terminal and invoicing software included

What we don't like

- Hardware selection is more limited than Square or Clover

- Lacks the massive third-party integration ecosystem of Stripe

Best for: Mid-sized businesses, medical offices, and B2B sellers seeking the absolute best transparent wholesale pricing.

Considering Helcim vs Square? Helcim's Interchange-Plus pricing will mathematically save any merchant processing over $5,000/month significantly more money than Square's flat rates.

A brilliantly transparent, volume-discounted Interchange-Plus processor with absolutely zero monthly overhead.

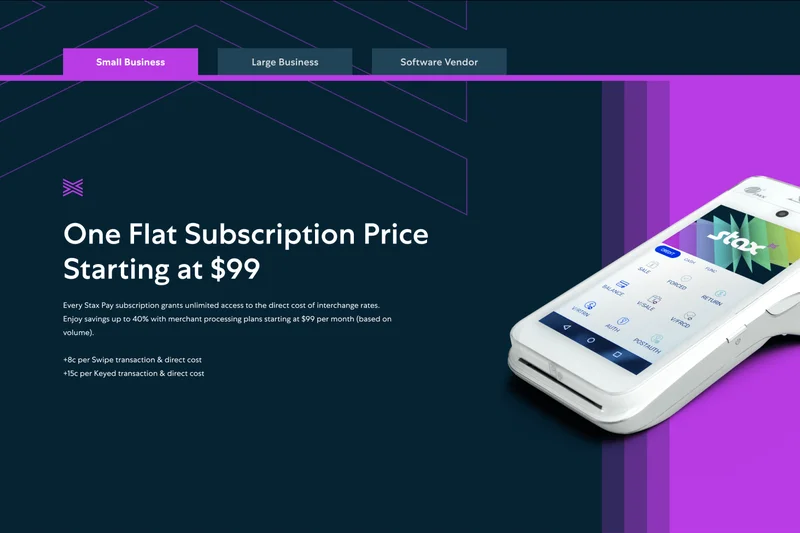

Buy at Helcim official site#17 Stax Payment Processing

Why we picked it: Stax disrupted the industry by pioneering the 0% markup wholesale subscription model. For a flat $99 monthly fee, merchants get direct access to raw wholesale interchange rates with zero percentage markup, paying only a tiny $0.08 fixed fee per transaction. For businesses processing over $15,000 to $20,000 a month, this mathematical structure saves thousands of dollars annually compared to flat-rate providers. Stax also provides an intuitive dashboard, free basic smart terminals, and next-day funding.

Key Specs

- 0% markup on wholesale interchange rates

- Predictable flat monthly subscription fee

- Free basic smart terminal included

- Next-day funding available

What we like

- Zero percentage markup on wholesale interchange rates saves fortunes

- Highly predictable flat monthly SaaS cost

- Excellent analytics dashboard and fast next-day funding

What we don't like

- The $99/mo fee makes it mathematically unviable for low-volume merchants

- Opaque underwriting standards for high-risk industries

Best for: Established, high-volume retail and B2B merchants processing in excess of $15,000 per month.

Considering Stax vs Stripe? If your average monthly volume exceeds $20k, Stax's monthly subscription model will drastically undercut Stripe's 2.9% flat rate, saving you massive profit margin.

A highly lucrative, zero-markup subscription processor designed mathematically to save high-volume merchants thousands of dollars.

Buy at Stax official site#18 Paddle Billing

Why we picked it: Paddle operates as a Merchant of Record (MoR), taking the immense legal and tax compliance burden entirely off the shoulders of SaaS and digital goods founders. When you use Paddle, they technically sell the product to the end user on your behalf, meaning they instantly handle all global VAT, sales tax remitting, and localized currency conversions out of the box. With powerful built-in dunning tools to reduce subscription churn, Paddle's slightly higher 5.0% + $0.50 rate is easily justified by the replacement of dedicated accounting and tax compliance teams.

Key Specs

- Complete global tax and VAT compliance

- Tailored SaaS subscription management

- Handles all fraud and chargeback disputes

- Automatic localized currency conversion

What we like

- Completely eliminates global sales tax and VAT compliance headaches

- Handles all chargeback disputes and fraud liability automatically

- Exceptional native SaaS subscription and dunning management

What we don't like

- 5.0% base transaction fee is significantly higher than standard gateways

- You technically hand over customer merchant-of-record control

Best for: Global SaaS startups, software developers, and digital creators who want to outsource international tax compliance.

Considering Paddle vs Stripe? While Stripe is cheaper, Paddle acts as your Merchant of Record, automatically calculating and remitting global VAT and sales tax so you don't have to hire international accountants.

The ultimate Merchant of Record platform that completely automates global tax compliance and subscription billing for software businesses.

Buy at Paddle official site#19 Lemon Squeezy MoR

Why we picked it: Lemon Squeezy has rapidly emerged as the most beautifully designed Merchant of Record (MoR) for digital creators and indie hackers. Similar to Paddle, it completely manages global tax and VAT compliance on digital goods. However, Lemon Squeezy distinguishes itself with a stunning, high-converting checkout UI, a native affiliate marketing platform out-of-the-box, and a secure software licensing API. For independent developers selling digital downloads, courses, or software keys, it provides an unparalleled, aesthetic, all-in-one business engine.

Key Specs

- Purpose-built for digital creators and software devs

- Fully managed global tax and VAT remitting

- Native affiliate marketing platform included

- Secure software licensing API out of the box

What we like

- Gorgeous, high-converting checkout experience

- Built-in software licensing API and affiliate marketing tools

- Completely offloads global tax and VAT liability

What we don't like

- High 5.0% + $0.50 transaction fee

- Strictly limited to digital products and software (no physical goods)

Best for: Indie hackers, digital creators, and software developers selling digital downloads or API keys globally.

Considering Lemon Squeezy vs Gumroad? Lemon Squeezy offers vastly superior checkout aesthetics, lower baseline fees, and much stronger API capabilities for custom software licensing.

A beautifully designed, all-in-one Merchant of Record and affiliate platform optimized perfectly for digital creators.

Buy at Lemon Squeezy official site#20 Payoneer Checkout

Why we picked it: Payoneer Checkout specializes in empowering cross-border e-commerce merchants and marketplace sellers. Known for its multi-currency receiving accounts, it allows sellers to accept payments globally and avoid massive conversion fees by holding USD, EUR, or GBP balances natively. Lightning-fast digital onboarding and deep integration with global marketplace payouts make it ideal for international dropshippers and remote contractors. Its ability to settle funds via direct local bank transfers in over 190 countries makes it an indispensable tool for borderless commerce.

Key Specs

- Multi-currency receiving accounts for global sellers

- Marketplace payout integration specialty

- Zero conversion fees on USD balances

- Supports direct local bank transfers globally

What we like

- Exceptional infrastructure for cross-border e-commerce and freelancers

- Multi-currency accounts avoid massive FX conversion loss

- Seamlessly integrates with major global marketplaces

What we don't like

- Base 3.0% transaction fee is slightly elevated

- Dashboard UI is somewhat dated compared to modern fintechs

Best for: International marketplace sellers, cross-border e-commerce brands, and global freelance agencies.

Considering Payoneer vs PayPal? Payoneer drastically outperforms PayPal in international B2B payouts, offering far better FX rates and localized bank transfer capabilities.

A robust cross-border gateway essential for international e-commerce sellers relying on multi-currency payouts.

Buy at Payoneer official site#21 WePay Platform Payments

Why we picked it: WePay, backed by the immense infrastructure of JPMorgan Chase, is a highly capable white-label processor built explicitly for embedded software platforms, crowdfunding sites, and vertical SaaS. It excels at instant, frictionless merchant onboarding APIs, allowing platforms to sign up sub-merchants in seconds while entirely offloading the complex KYC risk and compliance burdens. With the added benefit of same-day deposit availability via Chase, WePay is a quiet powerhouse running behind the scenes of many major SaaS tools.

Key Specs

- Deeply integrated with Chase bank infrastructure

- Ideal for embedded software platforms and crowdfunding

- Instant merchant onboarding APIs

- End-to-end risk and compliance managed

What we like

- Incredible instant API onboarding for platform sub-merchants

- Backed by the immense stability and liquidity of JPMorgan Chase

- Completely handles complex risk, KYC, and compliance for platforms

What we don't like

- Designed for platforms; not suitable for direct independent retailers

- API documentation is robust but less modern than Stripe's

Best for: Vertical SaaS platforms, donation portals, and crowdfunding sites wanting integrated white-label payments.

Considering WePay vs Stripe Connect? WePay leverages native Chase banking for faster settlements, though Stripe Connect offers a slightly more modern, internationally scalable API.

A rock-solid, Chase-backed white-label payment engine designed flawlessly for SaaS platforms and crowdfunding sites.

Buy at JPMorgan Chase official site#22 SeamlessChex Processing

Why we picked it: SeamlessChex Processing addresses the massive pain point of high-risk and high-volume merchants constantly facing sudden account freezes. With upfront, rigorous underwriting, SeamlessChex ensures that once you are approved, your funds flow without interruption. Utilizing deeply integrated Plaid APIs for instant bank verification, they boast an industry-leading 99.1% transaction acceptance rate for ACH processing, enforcing zero monthly volume caps and providing white-glove dedicated account management.

Key Specs

- Market-leading 99.1% transaction acceptance rate

- Upfront underwriting prevents sudden freezes

- No monthly processing volume caps

- Plaid integration for instant bank approvals

What we like

- Upfront manual underwriting virtually eliminates sudden account freezes

- Phenomenal 99.1% ACH acceptance rate using Plaid

- Dedicated, white-glove account managers actually answer the phone

What we don't like

- ACH settlement speeds are inherently slower than credit cards

- Initial onboarding process is lengthy and document-heavy

Best for: High-volume ACH billers and B2B merchants who need absolute protection against automated account freezes.

Considering SeamlessChex vs Stripe ACH? SeamlessChex relies on rigorous upfront human underwriting to guarantee your account won't be randomly frozen by an algorithm, unlike Stripe's automated risk model.

The premier high-volume ACH processor that trades a strict onboarding process for complete account stability and zero freezes.

Buy at SeamlessChex official site#23 Braintree Direct

Why we picked it: Acquired by PayPal, Braintree Direct is an API-first payment gateway that powers some of the largest mobile apps and digital platforms on earth. Its massive advantage is native, deep integration with the massive PayPal and Venmo consumer ecosystems, vastly improving checkout conversion rates for mobile users. Braintree offers highly customizable Drop-in UIs and adaptive advanced fraud management, making it an incredibly scalable, developer-friendly alternative for tech-forward enterprises.

Key Specs

- Native Venmo and PayPal ecosystem integration

- 130+ currencies supported

- Highly customizable Drop-in UI

- Adaptive advanced fraud management tools

What we like

- Native Venmo and PayPal integration drives huge mobile conversions

- Exceptional Drop-in UI and developer SDKs

- Highly adaptive fraud management tools included

What we don't like

- Account approval processes can be surprisingly rigid

- Customer support is often routed through slower tier-1 channels

Best for: Scaling mobile applications and e-commerce platforms that want native Venmo and PayPal routing.

Considering Braintree vs Stripe? Braintree's native inclusion of Venmo payment routing is a massive conversion booster for US-based mobile apps, though Stripe boasts a slightly broader global footprint.

An elite, developer-focused gateway that uniquely leverages the massive consumer reach of Venmo and PayPal.

Buy at PayPal official site#24 Payment Depot Processing

Why we picked it: Payment Depot operates on a highly lucrative subscription model, providing B2B and high-ticket merchants direct access to wholesale interchange pricing. By charging a flat $59 monthly fee, they completely eliminate the percentage markup that drains high-volume businesses. They are specifically notable for robust B2B Level 2 and 3 processing support, automatically optimizing corporate card transactions for the lowest possible interchange rates. With no cancellation fees and a free virtual terminal, it's a phenomenal B2B choice.

Key Specs

- Direct wholesale interchange pricing

- No cancellation or hidden fees

- Free virtual terminal and gateway

- B2B Level 2 and 3 processing support

What we like

- Zero percentage markup saves immense capital for high-ticket sellers

- Level 2 and 3 processing automatically lowers B2B corporate card rates

- Highly transparent terms with zero cancellation fees

What we don't like

- Requires consistent monthly volume to mathematically justify the $59 fee

- Dashboard and reporting UI is slightly dated

Best for: B2B merchants, wholesalers, and high-ticket retailers processing large average transaction sizes.

Considering Payment Depot vs Square? If your average transaction is over $500, Payment Depot's zero-markup model and Level 3 B2B optimization will vastly undercut Square's 2.6% fee.

An outstanding zero-markup subscription processor perfectly optimized to lower rates on high-ticket B2B transactions.

Buy at Payment Depot official site#25 Payline Data Services

Why we picked it: Payline Data Services is a highly respected Interchange-Plus processor with a strong specialization in medical billing, B2B services, and high-risk account operations. They provide incredibly transparent interchange-plus rates, avoiding all tiered pricing traps. What sets Payline apart is its native integration with QuickBooks and its dedication to providing highly responsive, US-based dedicated account managers, which is a rare luxury for mid-sized merchants navigating the complexities of high-risk or medical compliance processing.

Key Specs

- Medical and B2B processing specialization

- Transparent interchange-plus rates

- Native integration with QuickBooks

- Dedicated US-based account managers

What we like

- Exceptional transparent Interchange-Plus pricing model

- Specialized solutions for medical, B2B, and high-risk merchants

- Top-tier, dedicated US-based customer support teams

What we don't like

- Requires a $20 monthly gateway fee

- Lacks the polished, API-first onboarding flow of tech gateways

Best for: Medical practices, specialized B2B services, and mid-sized merchants prioritizing human customer support.

Considering Payline vs Stripe? Payline provides vastly superior human account management and high-risk industry support compared to Stripe's automated risk algorithms.

A highly transparent, reliably supported Interchange-Plus processor perfect for medical and B2B merchants.

Buy at Payline official site#26 Chase Payment Solutions

Why we picked it: Chase Payment Solutions bridges the gap between massive banking infrastructure and accessible small business payment processing. By operating as a direct bank processor, Chase offers a major cash-flow advantage: free, same-day deposits for businesses banking with Chase. Featuring no long-term contracts, predictable flat-rate pricing models (2.9% + $0.25/txn), and the ability to get in-person support at physical bank branches, it provides an unparalleled level of institutional trust and liquidity for local businesses.

Key Specs

- Free same-day deposits for Chase business accounts

- No long-term contracts required

- Built-in proprietary POS hardware options

- In-person support at physical bank branches

What we like

- Free same-day funding for Chase business checking account holders

- Backed by the immense security of the nation's largest bank

- Convenient in-person support at local retail branches

What we don't like

- Pricing is relatively standard flat-rate, not wholesale

- E-commerce API integrations are less nimble than fintech startups

Best for: Local businesses and professional services that already utilize Chase Business Banking.

Considering Chase vs Square? Chase offers the massive benefit of free same-day funding and in-branch support, assuming you hold a Chase business bank account.

A highly reliable, bank-direct payment processor offering unbeatable same-day funding for Chase customers.

Buy at Chase Bank official site#27 DOKU Payments Platform

Why we picked it: DOKU is the dominant payment processor within the booming Indonesian and broader Southeast Asian (SEA) markets. Western processors frequently fail in SEA due to low credit card penetration, but DOKU excels by deeply supporting major local e-wallets (OVO, Dana) and seamless virtual bank account transfers. With a heavily localized, advanced fraud detection engine trained specifically on SEA region heuristics, and robust recurring billing systems, DOKU is the undisputed gateway for conquering the archipelago.

Key Specs

- Dominant processor in the Indonesian market

- Supports all major local e-wallets (OVO, Dana)

- Deep virtual accounts integration

- Localized advanced fraud detection engine

What we like

- Absolute market dominance and localized trust in Indonesia

- Flawless native support for critical SEA e-wallets

- Advanced fraud engine customized for regional threats

What we don't like

- Highly localized; not suitable for merchants solely targeting the US/EU

- Custom volume pricing requires direct sales negotiation

Best for: Global brands, gaming platforms, and e-commerce companies aggressively expanding into Southeast Asia.

Considering DOKU vs Stripe? DOKU offers vastly superior conversion rates in Indonesia by natively supporting the virtual accounts and e-wallets that local consumers actually use.

The essential, hyper-localized payment gateway required to unlock massive scale in the Southeast Asian market.

Buy at DOKU official site#28 BlueSnap Global Gateway

Why we picked it: BlueSnap operates as an all-in-one payment orchestration platform, heavily optimized for B2B cross-border operations. It features intelligent multi-bank payment routing, which automatically sends transactions to the acquiring bank most likely to approve it, significantly boosting global authorization rates. Processing in over 100 shopper currencies and armed with advanced B2B Accounts Receivable automation and built-in global tax compliance, BlueSnap drastically simplifies international software and service sales.

Key Specs

- All-in-one payment orchestration platform

- Processes in 100+ shopper currencies

- Intelligent multi-bank payment routing

- Advanced B2B Accounts Receivable automation

What we like

- Intelligent multi-bank routing heavily reduces false declines globally

- Excellent built-in B2B accounts receivable and tax compliance

- Massive multi-currency shopper support

What we don't like

- The dashboard interface is complex and has a learning curve

- Integration requires moderate to heavy technical resources

Best for: International B2B software vendors and mid-market global e-commerce companies.

Considering BlueSnap vs PayPal? BlueSnap offers far superior B2B accounts receivable automation and intelligent global bank routing to ensure high-ticket approvals.

A highly intelligent global payment orchestrator built to maximize authorization rates and automate B2B invoicing.

Buy at BlueSnap official site#29 Dharma Merchant Processing

Why we picked it: Dharma is a certified B-Corp and stands out as the most ethical payment processor on the market. They offer heavily discounted, fully transparent interchange-plus processing rates explicitly tailored for non-profits and sustainable businesses. Operating with zero early termination fees, zero hidden markups, and exceptionally well-reviewed US-based B2B support, Dharma proves that payment processing can be both highly affordable and socially responsible. It is a phenomenal partner for organizations prioritizing transparency.

Key Specs

- Heavily discounted processing rates for non-profits

- Certified B-Corp payment processor

- Fully transparent interchange-plus pricing

- No early termination fees

What we like

- Industry-best discounted processing rates for non-profits

- Certified B-Corp committed to ethical, transparent business

- Exceptional human-led, US-based customer support

What we don't like

- Requires a $25 monthly fee

- Does not service high-risk industries or international merchants

Best for: Non-profits, charities, and ethical B2B merchants seeking transparent pricing and phenomenal support.

Considering Dharma vs Square? For non-profits processing large donation volumes, Dharma's specialized discount interchange rates will save thousands of dollars over Square's flat rates.

The premier ethical payment processor offering massive transparent discounts to non-profits and sustainable businesses.

Buy at Dharma official site#30 2Checkout Digital Commerce

Why we picked it: Acquired by Verifone, 2Checkout acts as a powerful Global Merchant of Record (MoR) gateway, specifically engineered to navigate the intense complexities of selling digital goods and software internationally. It automatically handles all global tax, VAT, and regulatory compliance on behalf of the merchant. Supporting over 45 international alternative payment methods and featuring deeply localized checkout experiences tailored to local buying habits, 2Checkout removes the massive legal overhead of global expansion.

Key Specs

- Handles global tax, VAT, and compliance

- Supports 45+ international payment methods

- Advanced subscription and recurring billing

- Specialized for digital goods and software

What we like

- Acts as MoR, completely offloading global tax and VAT compliance

- Excellent support for hyper-local international payment methods

- Deeply localized, conversion-optimized checkout UIs

What we don't like

- High 3.5% + $0.35 baseline fee cuts into margins

- UI and dashboard feel somewhat legacy compared to newer startups

Best for: Digital software companies and international service providers wanting zero global tax liability.

Considering 2Checkout vs Stripe? 2Checkout operates as an MoR, meaning they handle all global sales tax and VAT remittance for you, which Stripe does not natively do out of the box.

A robust, battle-tested Merchant of Record that seamlessly handles the legal and tax burdens of global digital sales.

Buy at Verifone official site#31 PayPal Checkout

Why we picked it: PayPal Checkout remains an absolute titan in the e-commerce world due to its unparalleled consumer brand trust and immediate global recognition. Integrating PayPal often provides an immediate conversion rate lift because millions of buyers already have their shipping and payment details vaulted. Offering completely frictionless, zero-code website integration, built-in Pay Later financing options, and the immensely popular Venmo integration, PayPal is an essential supplementary gateway for any modern online storefront.

Key Specs

- Highest consumer brand trust and recognition

- Global reach in 200+ countries

- Robust Seller Protection program

- Pay Later and Venmo integrations included

What we like

- Massive consumer trust drives immediate checkout conversions

- Includes powerful Pay Later financing options at no extra cost

- Incredibly simple zero-code implementation for basic sites

What we don't like

- High 3.49% + $0.49 per-transaction flat fee for digital checkouts

- Notorious for aggressive, automated account holds and freezes

Best for: Virtually all e-commerce merchants as a mandatory supplementary checkout option to boost conversions.

Considering PayPal vs Stripe? You should ideally use both. Stripe is better for your main white-labeled checkout API, while PayPal should be offered as an alternative trusted wallet button.

The globally trusted digital wallet that acts as an essential, high-converting checkout addition to any online store.

Buy at PayPal official site#32 RapidCents Gateway

Why we picked it: RapidCents is a rapidly emerging, highly capable e-commerce processor optimized specifically for North American merchants. It features extremely modern, developer-friendly APIs that make building custom e-commerce flows painless. RapidCents differentiates itself with real-time transaction monitoring, granular analytics, and customizable smart invoicing tools that support automated recurring payment schedules. It provides a highly stable, transparent flat-rate alternative for mid-market online sellers.

Key Specs

- Real-time transaction monitoring and analytics

- Customizable smart invoicing tools

- Automated recurring payment schedules

- Optimized for North American merchants

What we like

- Excellent real-time analytics and transaction tracking

- Modern, highly intuitive developer APIs and documentation

- Robust recurring payment and smart invoicing tools

What we don't like

- Primarily focused on the North American market; lacks deep global reach

- Brand recognition is lower than legacy Tier 1 gateways

Best for: North American e-commerce startups and mid-market merchants looking for a modern, analytics-rich gateway.

Considering RapidCents vs Authorize.net? RapidCents provides significantly more modern API architecture and far superior real-time analytics dashboards without the legacy clunkiness.

A nimble, highly analytical modern payment gateway tailored perfectly for North American e-commerce growth.

Buy at RapidCents official site#33 Elavon Merchant Services

Why we picked it: Backed by U.S. Bank, Elavon is a massive traditional direct acquirer and processor heavily relied upon by the travel, airline, and hospitality sectors. Because they own the entire processing network from end to end, they offer incredibly robust, custom omnichannel solutions and highly reliable next-day funding natively integrated with U.S. Bank. For massive physical enterprise operations requiring dedicated 24/7 customer service and complex high-volume custom routing, Elavon brings unmatched institutional stability.

Key Specs

- Direct acquirer and processor network

- Specialization in travel and hospitality sectors

- Next-day funding exclusively with U.S. Bank

- Dedicated 24/7 enterprise customer service

What we like

- Massive institutional stability and direct acquirer network speed

- Exceptional capabilities for travel, hotel, and restaurant chains

- Dedicated 24/7 enterprise-grade customer support

What we don't like

- Pricing is entirely custom and notoriously opaque for small businesses

- Legacy technology stack moves slower than modern fintechs

Best for: Enterprise hospitality brands, airlines, and massive retail chains requiring direct acquirer stability.

Considering Elavon vs Square? Elavon is engineered for massive corporate hospitality deployments requiring custom negotiated rates, whereas Square is built for immediate small business deployment.

An institutional powerhouse acquirer providing unmatched stability and custom routing for global hospitality enterprises.

Buy at U.S. Bank official site#34 Authorize.net Payment Gateway

Why we picked it: Owned and backed by Visa, Authorize.net is one of the oldest and most universally compatible traditional payment gateways on the internet. It acts as the ultimate reliable bridge, boasting thousands of legacy third-party software integrations that newer gateways simply do not support. Featuring an Advanced Fraud Detection Suite (AFDS) and a highly secure Customer Information Manager for vaulting profiles, it remains a steadfast, highly reliable workhorse for traditional B2B and e-commerce websites.

Key Specs

- Owned and backed by Visa infrastructure

- Advanced Fraud Detection Suite (AFDS)

- Customer Information Manager for vaulting

- Thousands of legacy 3rd-party software integrations

What we like

- Incredible compatibility with virtually every legacy software on earth

- Backed by the immense security infrastructure of Visa

- Excellent Advanced Fraud Detection Suite included

What we don't like

- Requires a $25 monthly fee plus per-transaction gateway costs

- Developer APIs and dashboard UI feel significantly dated

Best for: Established e-commerce sites and B2B portals utilizing legacy software that requires traditional gateway integration.

Considering Authorize.net vs Stripe? Authorize.net is necessary if your underlying ERP or legacy shopping cart lacks modern API support, while Stripe is far superior for new, custom-built applications.

The ultimate legacy workhorse gateway, offering unmatched universal compatibility and Visa-backed reliability.

Buy at Visa official site#35 Worldpay Integrated Payments

Why we picked it: Operated by FIS, Worldpay is a truly massive global payment processor renowned for its unmatched support of high-risk industries, gaming, and complex international deployments. Processing in over 120 currencies with advanced dynamic currency conversion (DCC), Worldpay handles billions of dollars seamlessly. It features highly advanced chargeback dispute management teams and comprehensive omnichannel SDKs for massive physical and digital enterprise integrations. While entirely unsuited for small businesses, its global acquiring scale is nearly peerless.

Key Specs

- Unmatched high-risk industry support

- 120+ processing currencies supported

- Dynamic currency conversion (DCC)

- Advanced chargeback dispute management

What we like

- Unmatched global acquiring network scaling across 120+ currencies

- Highly tolerant and specialized in complex, high-risk industries

- Exceptional dynamic currency conversion and chargeback handling

What we don't like

- Contracts are often multi-year with heavy early termination fees

- Small businesses receive notoriously slow tier-1 customer support